The landscape of American retirement is shifting as the provisions of the SECURE 2.0 Act take full effect in 2026. One of the most significant changes involves the aggressive integration of annuities into 401(k) plans. While the promise of a “guaranteed paycheck for life” sounds like the ultimate solution to longevity risk, recent data and market analysis suggest that these products may create a liquidity trap for the average saver. As of March 20, 2026, financial advisors and plan participants are beginning to grapple with the reality that what works for an insurance company’s bottom line might not align with a retiree’s need for flexibility.

The SECURE 2.0 Catalyst and the Push for Annuities

The rise of annuities within employer-sponsored plans isn’t accidental. Legislative updates, specifically the SECURE 2.0 Act, have provided employers with “safe harbor” protections. This legal shielding makes it significantly easier for plan sponsors to include annuity options without fearing litigation if an insurance company later fails to meet its obligations. Consequently, major financial institutions are pivoting their fulfillment strategies to include these insurance-linked products alongside traditional mutual funds and ETFs.

For the insurance industry, the 401(k) market represents a massive, largely untapped frontier. For the investor, however, the inclusion of an annuity in a tax-advantaged account like a 401(k) often results in redundant benefits and high “middleman” costs. The core appeal is the elimination of the fear of outliving one’s money, but the trade-off is often a loss of control over the principal investment.

The 83% Reality: Why Liquidity Matters Most

One of the most pressing concerns regarding the “annuitization” of retirement savings is the mismatch between fixed income and real-world expenses. According to recent data from March 2026, 83% of retirees face at least one major unexpected expense annually. These range from emergency home repairs and rising healthcare costs to supporting adult children through economic shifts.

When a participant rolls a significant portion of their 401(k) into an annuity, they are essentially trading a liquid asset for a contractually obligated stream of payments. While a monthly check provides stability, it lacks the elasticity required to handle a $15,000 roof replacement or a $20,000 medical deductible. Unlike a traditional 401(k) where funds can be withdrawn (subject to taxes and potential penalties), many annuities come with restrictive surrender charges.

Understanding the Cost of Certainty

The “guarantee” provided by an annuity is not free; it is a priced product. Variable annuities, which are increasingly common in modern 401(k) lineups, are notorious for their complex fee structures. Investors often encounter a “layering” effect where they pay administrative charges, mortality and expense risk charges (M&E), and investment management fees.

In many cases, these total fees can exceed 2% to 3% annually. To put that in perspective, a low-cost S&P 500 index fund in a standard 401(k) might have an expense ratio as low as 0.03%. Over a 20-year retirement horizon, that fee differential can result in hundreds of thousands of dollars in lost wealth. Furthermore, the SECURE 2.0 environment has led to more “embedded” fees that are difficult for the average participant to decipher without professional help.

If a retiree decides they need their principal back, they may hit the “surrender charge” wall. These charges can be as high as 10% of the total value in the early years of the contract. This lack of maneuverability is a primary reason why many fiduciary advisors suggest that investors maintain a healthy balance of liquid assets outside of any annuitized products.

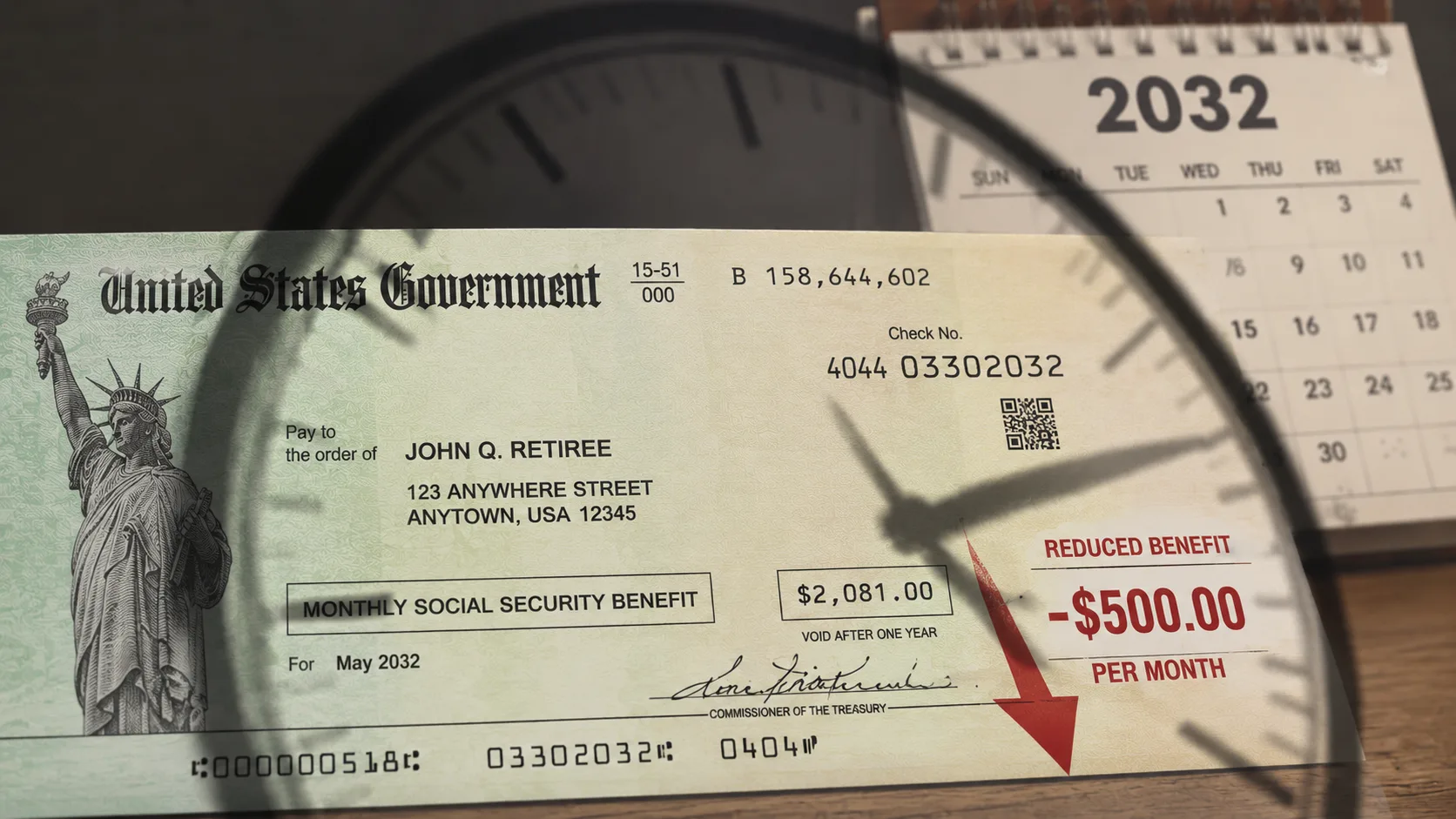

The Inflation Gap: A Silent Erosion of Wealth

A critical flaw in the majority of 401(k) annuities is the lack of inflation indexing. While some products offer inflation riders, these typically come at an even higher cost, further reducing the initial monthly payout. As we look at the economic climate in early 2026, the cost of living remains a top concern for those on fixed incomes.

Without an inflation adjustment, a $2,000 monthly payment today will have significantly less purchasing power in 15 or 20 years. Historical equity returns have averaged approximately 9.3% over the last 140 years, providing a natural: though volatile: hedge against inflation. By locking into a fixed annuity rate, a retiree effectively exits the growth engine of the global markets, trading potential upside for a nominal stability that may not keep pace with the rising price of eggs, electricity, or healthcare.

Redundancy and the Tax-Deferred Trap

One of the most misunderstood aspects of putting an annuity inside a 401(k) is the redundancy of tax benefits. An annuity is naturally a tax-deferred vehicle. A 401(k) is also a tax-deferred vehicle. Placing an annuity inside a 401(k) is often described by critics as “wearing two raincoats.” You aren’t getting double the tax protection; you are simply paying the fees of an insurance product to get a benefit you already possessed through the retirement account structure itself.

Furthermore, annuities within 401(k)s often offer “death benefits” that guarantee your beneficiaries will receive at least the amount you invested. However, in a standard 401(k) invested in a diversified portfolio, the beneficiaries simply inherit the remaining balance of the account anyway. Paying an extra 1% or more in fees for a death benefit on a retirement account is often an unnecessary drain on the participant’s living expenses.

Conflicts of Interest in Plan Menus

The transition toward annuities in employer plans has also raised questions about conflicts of interest. Insurance companies that administer these plans have a clear financial incentive to steer participants toward high-fee insurance products rather than low-cost mutual funds. These companies often profit on both sides: they collect the fees for managing the 401(k) platform and the premiums for the annuity contracts.

While the Department of Labor has historically sought to enforce a fiduciary standard, the safe harbor provisions of SECURE 2.0 have created a more permissive environment for these products. Investors must be aware that the presence of an annuity on their 401(k) menu is not necessarily an endorsement of its value relative to other options. It may simply be the result of a negotiated package between the employer and the plan provider.

Balancing the Strategy: A Middle Ground

For most investors at Global Market News, the most effective retirement strategy involves balance rather than an “all or nothing” approach to annuitization. Financial experts suggest that if an investor is worried about outliving their money, they should first maximize their Social Security benefits: which are essentially a government-backed, inflation-adjusted annuity.

If additional guaranteed income is needed, it may be more efficient to purchase a low-cost Immediate Annuity (SPIA) with a small portion of one’s savings at the actual time of retirement, rather than locking into a complex variable annuity inside a 401(k) during the accumulation phase. This keeps the majority of the retirement nest egg in liquid, growth-oriented investments like equities and bonds, where fees are transparent and liquidity is maintained for those 83% of unexpected life events.

What It Means for Plan Participants

As 2026 progresses, plan participants should expect to see more marketing materials highlighting “lifetime income options.” The language will be persuasive, focusing on the peace of mind and the elimination of market volatility. However, the data suggests that for many, the “annuity trap” is a high price to pay for that peace.

Before committing to an annuity option within a 401(k), investors should ask three specific questions:

- What is the total all-in fee, including M&E and administrative charges?

- What is the surrender schedule if I need to withdraw my principal in three years?

- Is this payment adjusted for inflation, and if not, how will my purchasing power be protected?

The shift toward these products signals that the financial services industry believes the future of retirement is “insured.” Whether that insurance is worth the cost of lost growth and limited liquidity is a question every investor needs to answer before they sign on the dotted line. For more insights on navigating these changes, visit Global Market News.

The Bottom Line on Retirement Security

The move toward annuities in 401(k) plans is a response to a very real fear: the fear of the “zero balance.” While the insurance industry has provided a tool to address that fear, it is a tool with significant sharp edges. Between the 10% surrender charges, the 83% likelihood of needing emergency cash, and the erosion of wealth via un-indexed payments, the “guaranteed income” dream can quickly turn into a financial bottleneck.

The trend indicates that while the industry is pushing for more “guarantees,” the most successful retirees will likely be those who maintain their flexibility. As SECURE 2.0 continues to reshape the retirement landscape, staying informed about the hidden costs of these “safe” products is the best way to ensure that your golden years are actually spent on your own terms.