A new study from Northwestern Mutual found that the average “magic number” Americans believe they need for retirement has jumped to $1.46 million in 2026, up roughly $200,000 from the prior year.

Why the “Magic Number” Keeps Rising

Several major forces are driving Americans to increase their retirement targets:

1. Inflation Is Still Reshaping Expectations

Even as inflation has cooled from its peak, prices remain elevated across essentials like housing, food, and healthcare. For retirees living on fixed income, this creates a major planning challenge.

2. Americans Are Living Longer

The U.S. is currently in a demographic wave often referred to as “Peak 65,” where more than 10,000 Americans turn 65 every day through 2027. Longer life spans mean retirement savings must stretch further than ever before.

3. AI Is Creating Job Anxiety

Concerns about artificial intelligence are no longer theoretical. Roughly one-third of Americans say they are pessimistic about AI’s impact on their careers, with that number rising to nearly half among younger workers.

4. Social Security Uncertainty

The future of Social Security Administration remains a major concern. Without legislative changes, projections show the system could face benefit reductions of around 24% by 2032.

As Northwestern Mutual’s Chief Field Officer John Roberts explained:

“The new ‘magic number’ reflects a convergence of factors — from persistent inflation and longer life expectancies, to uncertainty about the future of Social Security.”

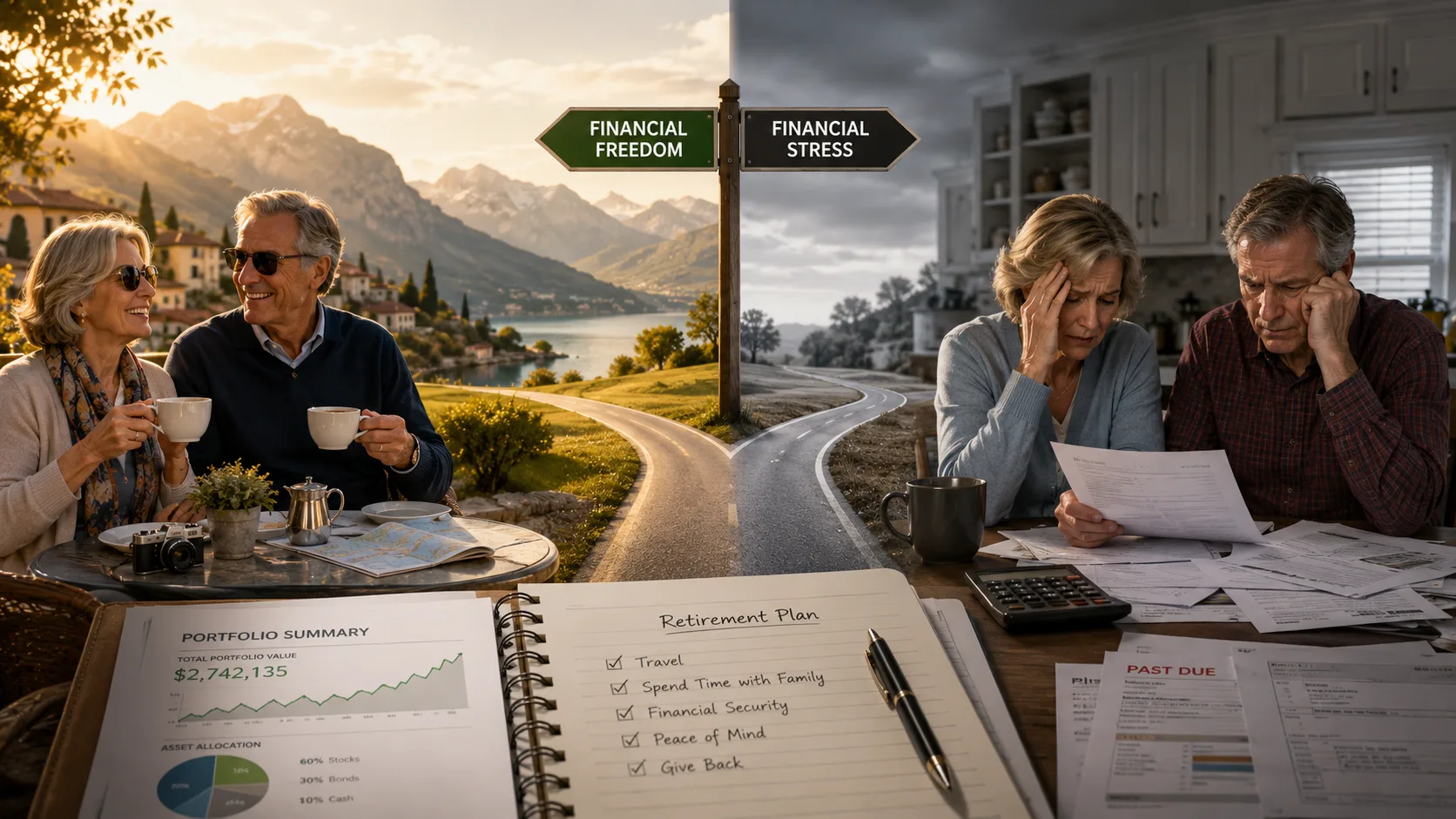

The Reality Check: Most Americans Are Far Behind

Here is where things get uncomfortable.

While Americans think they need $1.46 million, most are nowhere close.

Data from the National Institute on Retirement Security shows:

- Median retirement savings across all workers: $955

- Median savings for those with retirement accounts: $40,000

That is not a gap. That is a canyon.

Nearly 46% of Americans say they do not expect to be financially prepared for retirement, and the concern is justified.

Roberts put it bluntly:

“There’s a widening gap between what people have versus what they need. There’s an epidemic of financial anxiety.”

High-Net-Worth Americans Expect Even More

Even those who are ahead financially are raising their expectations.

Americans with over $1 million in investable assets believe they will need $2.67 million on average to retire comfortably.

That signals something important for investors:

- Wealth does not eliminate uncertainty

- It often increases awareness of long-term risks

The Hidden Cost That Can Break Retirement Plans

One of the biggest overlooked factors is healthcare.

According to Fidelity Investments, a 65-year-old retiring in 2025 can expect to spend approximately:

- $172,500 on healthcare expenses during retirement

And that number does not include long-term care events, which can easily push total costs into the hundreds of thousands more.

This is one of the biggest reasons traditional retirement estimates often fall short.

Why $1.46 Million May Still Not Be Enough

Even if someone hits the new “magic number,” it may not deliver the lifestyle they expect.

A common guideline is the 4% rule, which suggests withdrawing 4% of your savings annually.

On $1.46 million, that produces:

- About $58,000 per year in income

For many households, that is not enough to comfortably cover:

- Housing

- Healthcare

- Inflation-adjusted living expenses

- Unexpected costs

Roberts acknowledged this limitation:

“It may seem like a massive number at $1.46 million, but on the other hand, it may not be enough.”

Americans Fear Running Out of Money

The psychological pressure is building.

- 48% of Americans believe they could outlive their savings

- That rises to 55% for millennials

- And 50% for Gen X

Yet despite these fears:

- 36% of Americans have taken no action to address the risk

That disconnect between fear and action is one of the biggest risks in the system.

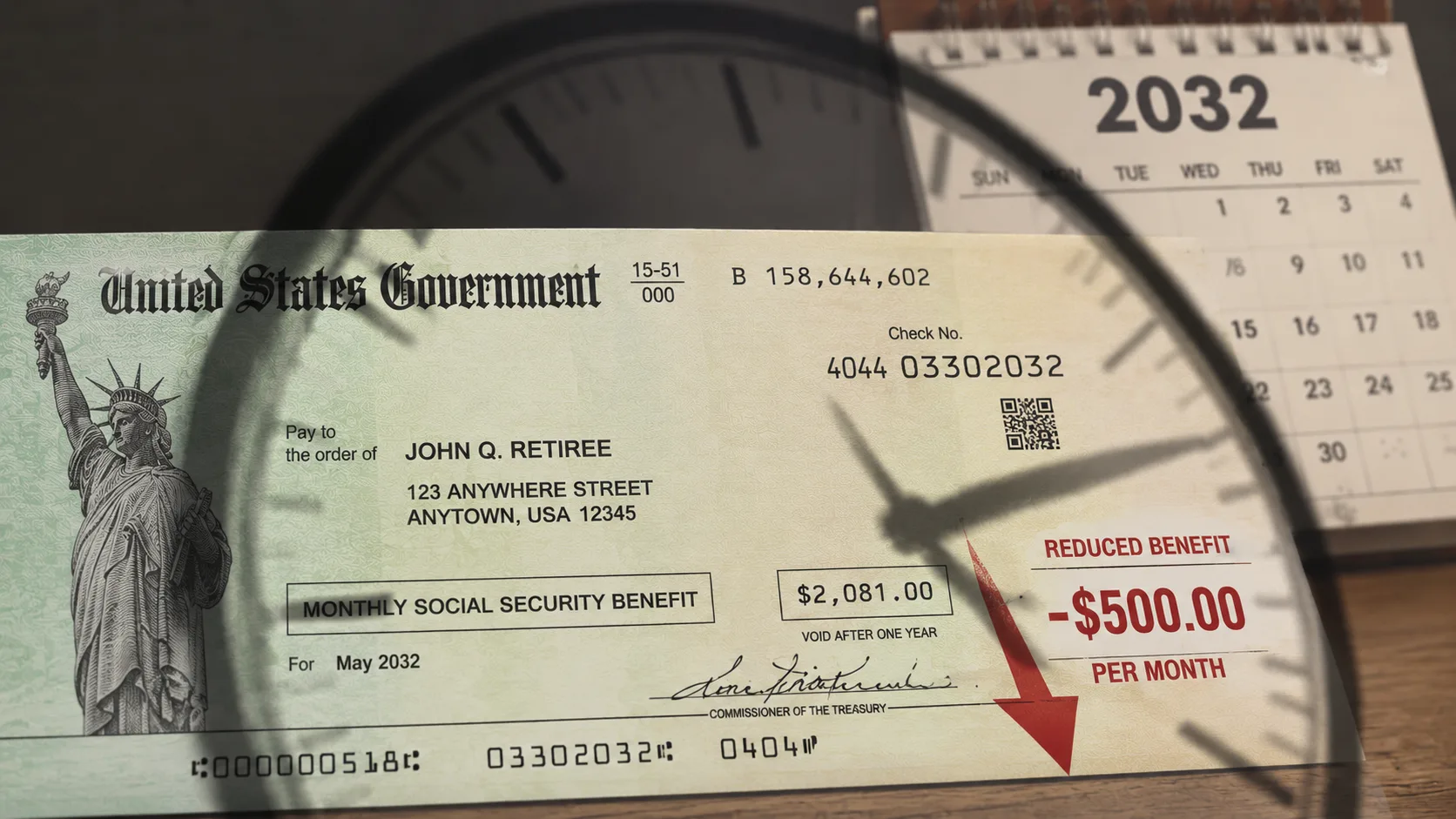

The Social Security Wild Card

Right now, the average monthly Social Security benefit is about:

- $2,076 per month (2026)

That equals roughly $24,900 per year.

Even combined with retirement savings, that may not be enough for many households — especially if benefit cuts occur in the next decade.

For investors, this creates a clear takeaway:

Relying on Social Security alone is not a strategy. It is a risk.

What This Means for Investors Right Now

This trend is not just a personal finance story. It is a market signal.

Here is how to think about it:

1. Retirement Is Becoming an Investment Problem, Not Just a Savings Problem

Traditional saving alone is unlikely to bridge the gap. Investors will need growth, income, and diversification.

2. Income-Producing Assets Will Become More Important

Dividend stocks, bonds, and alternative income strategies may see increased demand.

3. Healthcare and Longevity Industries Benefit

As retirement spans extend, sectors tied to aging populations could see long-term tailwinds.

4. Financial Services Demand Will Rise

Advisors, retirement planning tools, and wealth management platforms are positioned to grow as complexity increases.

The Bottom Line

The headline number is simple: $1.46 million.

But the real story is much bigger.

Americans are waking up to a harsh reality:

- Retirement is more expensive

- It lasts longer

- And the safety nets are less certain

The danger is not just that people are underprepared.

It is that many still have not adjusted their strategy to match this new reality.