Many Americans glance at the retirement income estimate on their 401(k) statement and assume that’s what they’ll actually have to live on. But experts say that number may dramatically understate your future retirement income, potentially discouraging millions of workers from saving enough for retirement.

For younger investors in particular, the estimate printed on many annual 401(k) statements can paint an unnecessarily bleak picture because of how federal regulations require those projections to be calculated.

Key Takeaways

- Current 401(k) statements estimate retirement income using only your current account balance.

- Required projections assume you never make another contribution before retirement.

- Younger workers may see retirement income estimates that are far lower than what they could realistically achieve.

- Experts argue more realistic projections could encourage higher retirement savings.

Why Your 401(k) Statement May Be Giving You the Wrong Impression

Since passage of the SECURE Act of 2019, employers have been required to include an estimate of future monthly retirement income on annual 401(k) benefit statements.

The goal was simple: help workers understand what their retirement savings might actually provide once they stop working.

While the requirement represented a major step forward for retirement planning, many financial experts believe there’s one major flaw.

The required estimate is based almost entirely on your current account balance, assuming you stop contributing immediately and never invest another dollar before retirement.

For most workers, that’s an unrealistic assumption.

The Missing Piece That Changes Everything

Most people contribute to their 401(k) for decades.

Employees continue making payroll deductions, employers often provide matching contributions, investments have years to compound, and many workers increase contributions as their income rises.

Yet none of those factors are reflected in the standard retirement income estimate required on many statements.

As a result, younger workers often receive projections that appear surprisingly small.

Instead of motivating additional saving, some experts worry those estimates could have the opposite effect.

If retirement appears to produce only a modest monthly income despite years of saving, some workers may question whether increasing contributions is even worthwhile.

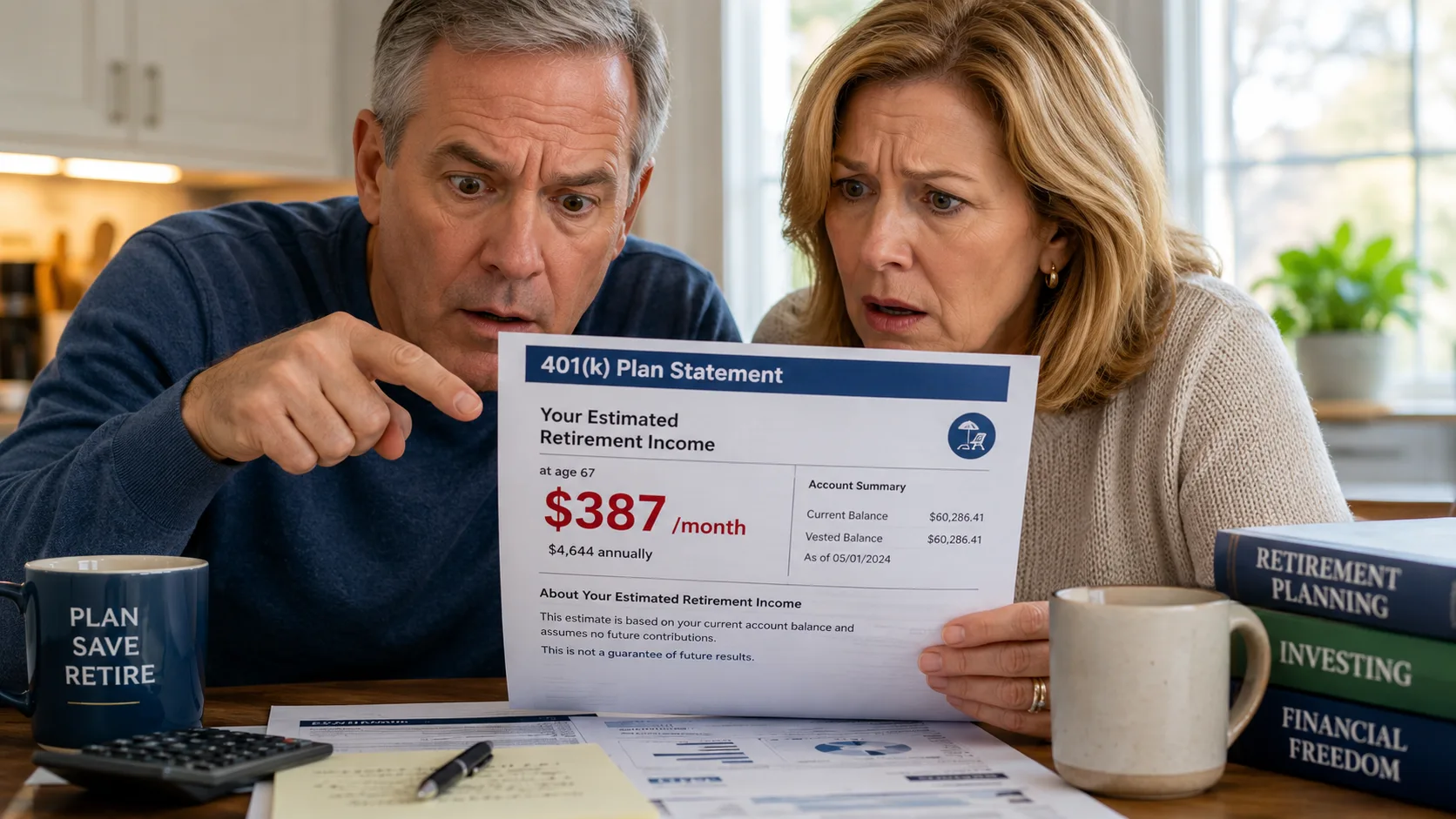

A Real-World Example

Consider a hypothetical 31-year-old employee:

- Annual salary: $75,000

- Current 401(k) balance: $60,000

- Retirement age: 67

Using today’s required methodology, that balance might generate an estimated retirement income of roughly $4,000 per year.

At first glance, that number appears discouraging.

However, it ignores another 36 years of:

- Employee contributions

- Potential employer matching

- Market growth

- Compound returns

When those factors are incorporated using reasonable assumptions, projected annual retirement income can exceed $40,000 per year—more than 10 times higher than the figure shown on many required statements.

That difference illustrates how dramatically assumptions can change long-term retirement projections.

Why This Matters for Younger Investors

Behavioral finance research has consistently shown that investors are more likely to save when they understand the long-term impact of their decisions.

Seeing an unrealistically low retirement estimate could unintentionally discourage workers who are decades away from retirement.

For someone in their 20s or early 30s, the majority of their retirement wealth has yet to be accumulated.

Future contributions and decades of investment growth often account for a much larger portion of retirement assets than the money already saved.

Without including those factors, many retirement projections fail to reflect what workers are actually building over time.

Some Providers Already Offer Better Tools

Not every retirement plan is limited to the minimum federal requirement.

Many large 401(k) providers already offer interactive retirement planning calculators that include assumptions for:

- Future salary increases

- Ongoing employee contributions

- Employer matching

- Expected investment returns

- Different retirement ages

Some even allow participants to adjust variables themselves.

Workers can test questions like:

- What happens if I increase my contribution by 2%?

- What if I retire two years later?

- How much difference could stronger investment returns make?

These planning tools often provide a much more realistic picture of retirement readiness.

The challenge is that many younger workers never use them.

Instead, they rely solely on the income estimate printed on their annual statement.

Could Federal Rules Eventually Change?

Some retirement experts believe future regulations should require projections that better reflect how people actually save.

Rather than assuming contributions stop immediately, standardized estimates could include reasonable assumptions for continued saving, salary growth and long-term investment returns.

Supporters argue that providing more realistic projections would give workers a clearer understanding of how today’s savings decisions affect tomorrow’s retirement income.

Critics note that adding assumptions introduces uncertainty because every investor’s future will differ.

Still, many believe a projection based on realistic saving behavior would be more useful than one based on an assumption almost no worker actually follows.

What Investors Should Do Instead

Whether you’re 25 or 55, it’s important to remember that the retirement income estimate on your 401(k) statement is only one snapshot—not a prediction of your financial future.

If you’re decades away from retirement, your actual retirement income will likely depend far more on:

- Continuing regular contributions

- Increasing savings as your income grows

- Employer matching contributions

- Long-term investment performance

- How long you remain invested

Looking beyond the standard estimate and using more comprehensive retirement planning tools can provide a far better understanding of where you’re actually headed.

The Bottom Line

The retirement income estimate on your annual 401(k) statement may be technically accurate under current federal rules, but it often fails to reflect how people actually build wealth over a lifetime.

For younger investors especially, the number can dramatically understate future retirement income because it assumes saving stops today.

Understanding what the estimate leaves out—and focusing on long-term contributions and compound growth rather than a single printed figure—can help investors make more informed decisions and stay committed to building retirement security over the decades ahead.