Millions of retirees spend decades building their nest eggs, only to discover an unpleasant surprise after they stop working: taking money from retirement accounts can trigger a hidden tax penalty that dramatically increases what they owe the government.

Financial planners call it the “Social Security Tax Torpedo.”

And for some retirees, it can push their effective tax rate above 40%—even if they’re nowhere near the highest tax brackets.

The problem isn’t simply paying taxes on retirement withdrawals. It’s the way Social Security benefits, required minimum distributions (RMDs), and Medicare premiums interact to create a retirement tax burden that many Americans never see coming.

Why Some Retirees Pay Zero Taxes While Others Pay Thousands

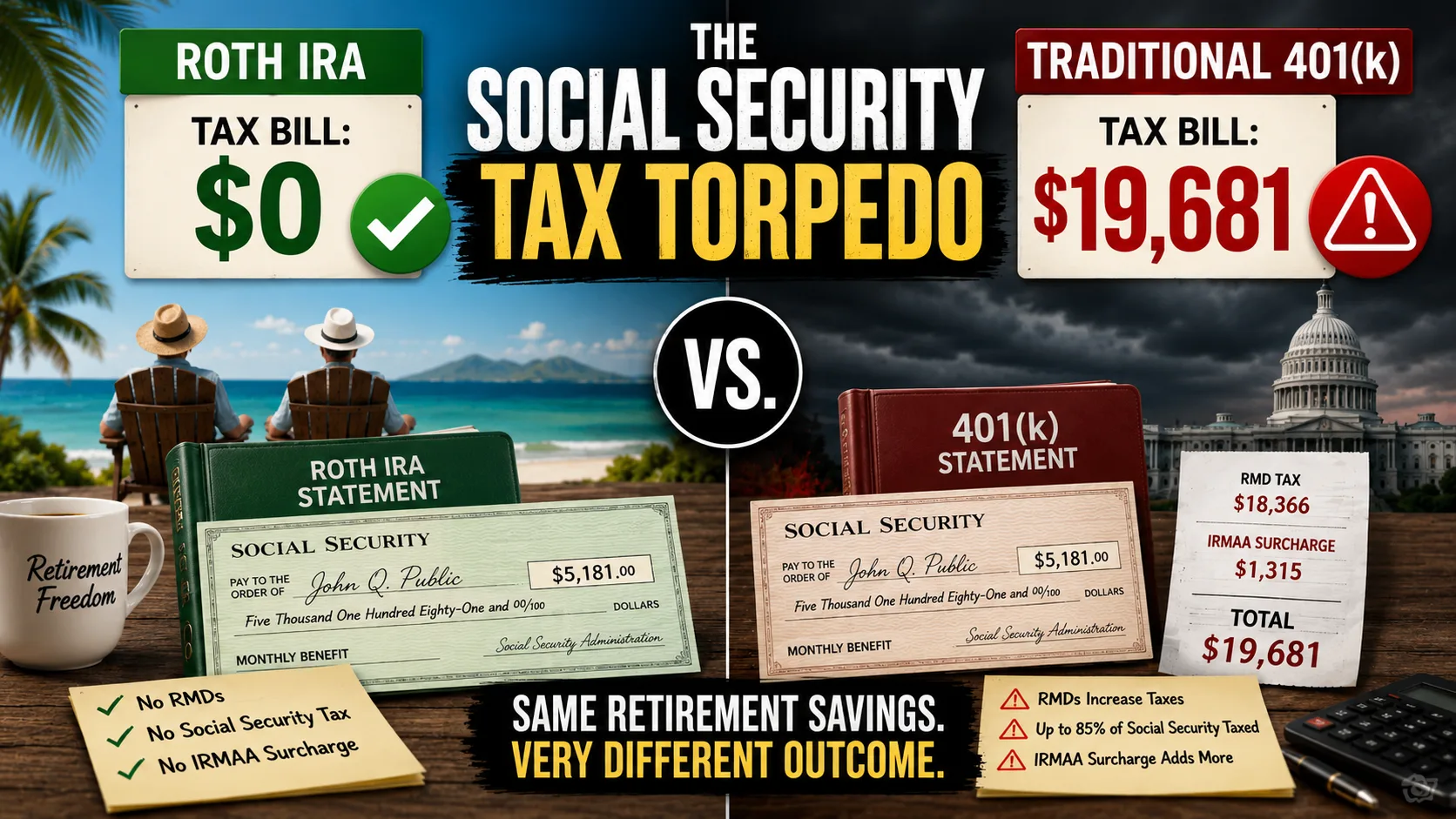

Imagine two retirees who both receive the maximum Social Security benefit.

One has accumulated $2 million inside a Roth IRA.

The other has accumulated $2 million inside a traditional 401(k).

On paper, both retirees have the same net worth.

But their tax bills look dramatically different.

The retiree with the Roth account can withdraw money tax-free and receives Social Security benefits without triggering additional federal income taxes.

The retiree with the traditional 401(k) faces a different reality.

Beginning at age 73, required minimum distributions force withdrawals from the account. Those withdrawals count as ordinary taxable income and can trigger taxation of Social Security benefits.

According to calculations from retired finance professor William Reichenstein, a retiree receiving the maximum Social Security benefit and taking a required minimum distribution from a $2 million tax-deferred account could owe roughly $18,000 annually in federal taxes.

And that’s before factoring in Medicare surcharges.

What Is the Social Security Tax Torpedo?

Most retirees assume Social Security is either taxable or tax-free.

The truth is more complicated.

The government uses a formula called “provisional income” to determine whether your benefits become taxable.

Provisional income includes:

- Taxable retirement withdrawals

- Pension income

- Interest income

- Municipal bond interest

- Half of your Social Security benefits

Once provisional income crosses certain thresholds, the IRS begins taxing a portion of your Social Security benefits.

For married couples, the key threshold is $44,000.

For single filers, it’s $34,000.

Above those levels, up to 85% of Social Security benefits can become taxable.

The result is what planners refer to as the tax torpedo.

Each additional dollar of retirement income can cause more of your Social Security benefit to become taxable at the same time.

Instead of paying taxes on just the new income, retirees can effectively pay taxes on both the withdrawal and a larger portion of their Social Security check.

How a 22% Tax Bracket Can Turn Into a 40% Tax Rate

This is where things become particularly painful.

Many retirees believe they’re safely sitting inside the 22% federal tax bracket.

But marginal tax rates and effective tax rates are not always the same thing.

Because every additional dollar withdrawn from a retirement account can trigger taxation of additional Social Security income, the real tax impact can be much higher than the official tax bracket suggests.

Reichenstein estimates that some retirees can face effective marginal tax rates exceeding 40%.

For certain married couples, the figure can approach 46% when other retirement tax provisions are factored in.

In other words, retirees may surrender nearly half of every additional dollar they withdraw—even though they are nowhere near the top federal tax bracket.

The Medicare Surcharge Most Retirees Overlook

The tax torpedo isn’t the only issue.

Higher retirement income can also trigger Income-Related Monthly Adjustment Amounts, commonly known as IRMAA.

IRMAA increases Medicare Part B and Part D premiums for retirees whose income exceeds certain thresholds.

While technically not a tax, the effect is similar.

As income rises, retirees send more money to the federal government through higher Medicare costs.

For retirees taking large RMDs, these premium increases can continue for years because required withdrawals generally rise as account balances remain substantial and life-expectancy factors decline.

What starts as a retirement withdrawal strategy can eventually become a permanent increase in healthcare costs.

Why Roth Accounts Are Becoming More Valuable

The growing popularity of Roth accounts is not just about tax-free withdrawals.

For many retirees, Roth assets can help avoid the chain reaction that creates the tax torpedo.

Qualified Roth withdrawals are generally not counted as taxable income.

That means retirees can access cash without increasing provisional income, triggering Social Security taxation, or pushing themselves into higher Medicare premium brackets.

Consider a married couple receiving more than $120,000 annually in Social Security benefits and holding $3 million in retirement savings.

If those assets sit entirely inside Roth accounts, they may owe little to no federal income tax on retirement withdrawals.

If those same assets are held in traditional tax-deferred accounts, required minimum distributions could generate tax bills approaching $30,000 annually.

The difference can add up to hundreds of thousands of dollars over the course of retirement.

The Roth Conversion Window Many Retirees Miss

One of the most powerful opportunities for retirement tax planning often occurs between retirement and the start of Social Security benefits.

During this period, retirees may temporarily find themselves in lower tax brackets.

That creates an opportunity to convert portions of traditional retirement accounts into Roth accounts while paying taxes at potentially lower rates.

By reducing future tax-deferred balances, retirees can shrink future RMDs and potentially avoid much of the Social Security tax torpedo later in life.

The strategy isn’t right for everyone.

But for retirees with large traditional IRA or 401(k) balances, the years before Social Security and RMDs begin may represent one of the most valuable tax-planning windows available.

What Investors Should Do Now

The Social Security tax torpedo catches many retirees by surprise because it doesn’t appear on account statements and receives far less attention than investment returns.

Yet for many households, retirement taxes can have just as much impact on long-term wealth as portfolio performance.

Investors approaching retirement should evaluate:

- Expected Social Security benefits

- Future required minimum distributions

- Potential Medicare IRMAA exposure

- Roth conversion opportunities

- The mix between taxable, tax-deferred, and Roth assets

The goal isn’t necessarily to eliminate taxes.

It’s to avoid accidentally triggering a retirement tax trap that can dramatically reduce the income your portfolio ultimately produces.

For retirees who have spent decades building wealth, understanding the Social Security tax torpedo may be just as important as deciding where to invest in the first place.