A new survey from the Employee Benefit Research Institute (EBRI) shows that Americans are increasingly uncertain about their ability to retire comfortably. The findings reflect growing anxiety tied to inflation, government policy risks, and shifting economic conditions that continue to pressure household budgets.

The data paints a clear picture. Confidence is declining, costs are rising, and more Americans are adjusting their financial behavior in ways that could reshape markets in the years ahead.

Retirement Confidence Hits Multi-Year Lows

According to the latest EBRI Retirement Confidence Survey, only 61% of workers say they are very or somewhat confident they will have enough money to live comfortably in retirement.

That is a sharp drop from 67% in 2025 and well below the recent peak of 72% recorded in 2021. It also marks the lowest level of confidence seen in nearly a decade.

This decline comes despite a strong run in equity markets over the past few years. In theory, rising stock portfolios should improve retirement outlooks. In reality, rising costs are overshadowing those gains.

Craig Copeland, director of wealth benefits research at EBRI, explained that inflation has become the dominant concern shaping how Americans think about retirement. Even households that have seen portfolio growth are feeling financially squeezed.

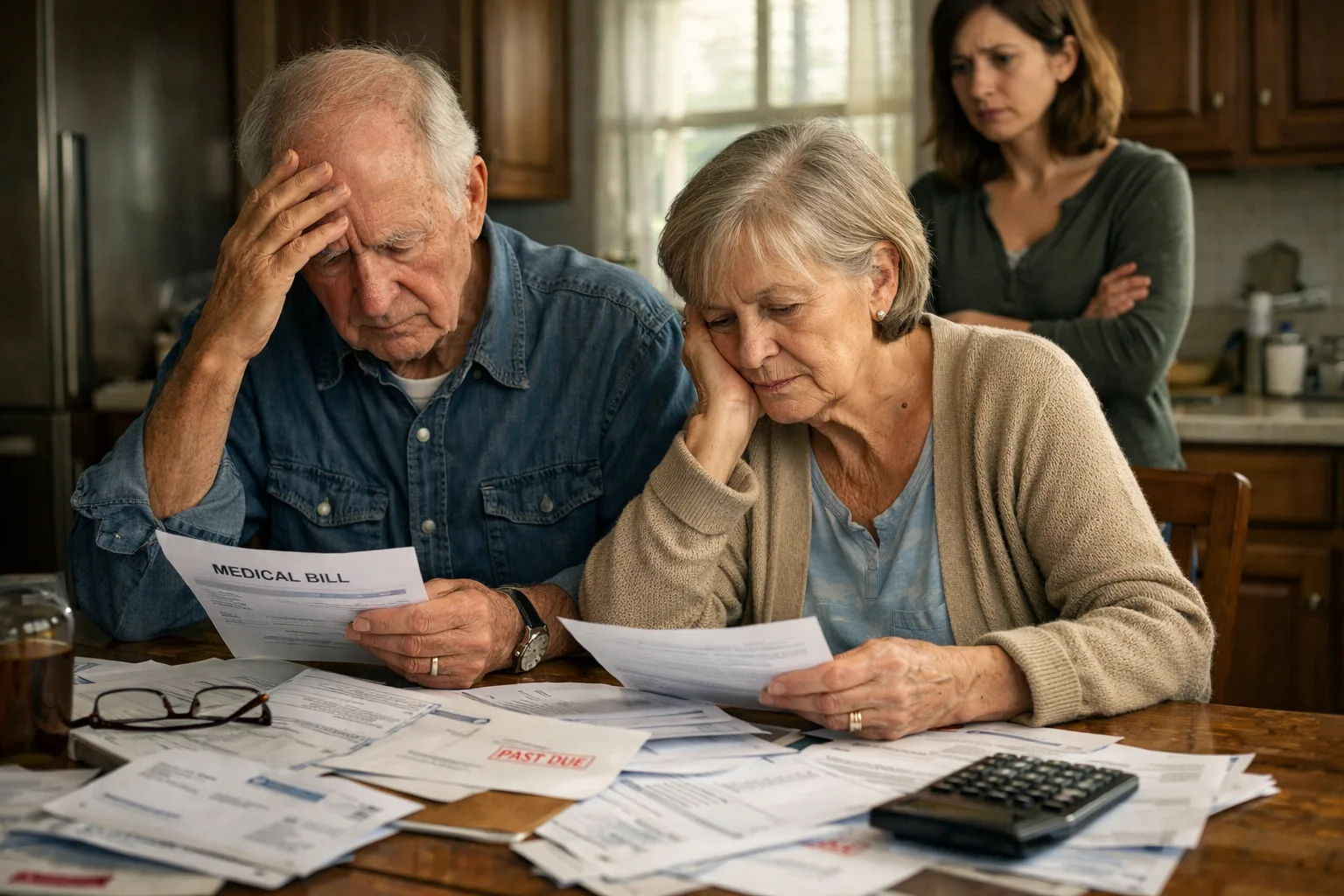

Inflation Is Quietly Undermining Retirement Plans

Inflation remains one of the most powerful forces eroding retirement confidence.

Many retirees and near-retirees are finding that their actual expenses are rising much faster than expected. Everyday essentials such as groceries, gasoline, healthcare, and insurance are all becoming more expensive.

One retiree, Janet Kieffer, said her spending has increased roughly 20% over the past year alone. Costs tied to healthcare have been particularly painful, including a recent $400 expense for a single medication.

This kind of cost pressure is not isolated. It is becoming increasingly common across the country.

The EBRI survey found that 41% of retirees say their spending is higher than they originally expected when they first retired. That is a major warning sign. Retirement planning models are being disrupted in real time.

More Retirees Are Looking for Income Again

One of the most telling shifts is behavioral.

More retirees are returning to work or seeking alternative income streams. Kieffer noted that many of her peers are now exploring ways to generate supplemental income, including part-time work or small business opportunities.

This trend reflects a broader shift. Retirement is no longer a static phase of life. For many Americans, it is becoming a dynamic financial balancing act.

From an investor perspective, this has ripple effects. Increased labor participation among retirees can impact wage trends, consumer spending patterns, and even demand for certain sectors such as gig economy platforms and small business tools.

Retirees Still More Confident Than Workers — But That Gap Is Narrowing

Historically, retirees have reported higher confidence than workers when it comes to financial security. That remains true, but even that confidence is starting to weaken.

The survey shows that 73% of retirees feel confident about their financial situation. While that is higher than workers, it is down from 78% just one year ago.

Workers, on the other hand, face more uncertainty. With retirement still years or decades away, they must contend with unknowns around job stability, healthcare costs, and long-term market performance.

The combination of falling confidence among both groups suggests a broader shift in sentiment that could persist for years.

Government Programs Are a Growing Concern

Beyond inflation, one of the biggest drivers of anxiety is the future of Social Security and Medicare.

Both workers and retirees expressed concern that these programs may face funding challenges in the coming years. Current projections indicate that, without reforms, key trust funds could face depletion around the mid-2030s.

That timeline is close enough to influence behavior today.

Financial adviser Jim Claire noted that many of his clients are choosing to claim Social Security benefits as early as possible.

“We fear the government will change the benefit rules if we wait too long,” he said. “We’d rather take the lower benefit amount early and invest it ourselves.”

This shift toward early claiming could have long-term implications for both individual wealth outcomes and government program sustainability.

Political and Economic Uncertainty Is Adding Fuel to the Fire

Recent political tensions and economic uncertainties are amplifying these concerns.

Government funding disputes and policy uncertainty have drawn more attention to the stability of federal programs. At the same time, geopolitical risks, including ongoing tensions involving Iran, are weighing on broader economic sentiment.

A separate survey from the University of Michigan recently showed consumer sentiment falling to one of its lowest levels in decades. While the EBRI survey was conducted earlier in the year, the broader trend is clear. Confidence across multiple dimensions is weakening.

For investors, this matters. Consumer sentiment often acts as a leading indicator for spending behavior, which drives a significant portion of economic growth.

What This Means for Investors

The decline in retirement confidence is not just a personal finance story. It is a market story.

Here are several key takeaways investors should be watching closely:

1. Increased Demand for Income-Producing Assets

As Americans seek more reliable income streams, demand for dividend-paying stocks, bonds, and alternative income investments could rise.

2. Growth in Retirement and Financial Planning Services

Companies that help individuals manage retirement risk, including financial advisory firms and fintech platforms, may see increased demand.

3. Pressure on Consumer Spending

Higher living costs and lower confidence can lead to more cautious spending behavior, which could impact sectors like retail, travel, and discretionary goods.

4. Policy-Driven Market Volatility

Concerns about Social Security and Medicare reforms could create uncertainty in markets, particularly in sectors tied to healthcare and government spending.

5. Longer Workforce Participation

More Americans working later in life could influence labor markets, wage growth, and productivity trends.

The Bottom Line

The message from the latest data is clear. Americans are becoming less confident about retirement, and the reasons are structural, not temporary.

Inflation, policy uncertainty, and shifting economic conditions are all converging to reshape how people think about their financial future.