The United States is on track for what economists call the “great wealth transfer,” with an estimated $72.6 trillion expected to pass from older generations to younger heirs over the coming decades. On paper, that should create one of the largest generational financial shifts in history.

But there’s a growing threat quietly eating away at that future wealth: long-term care costs.

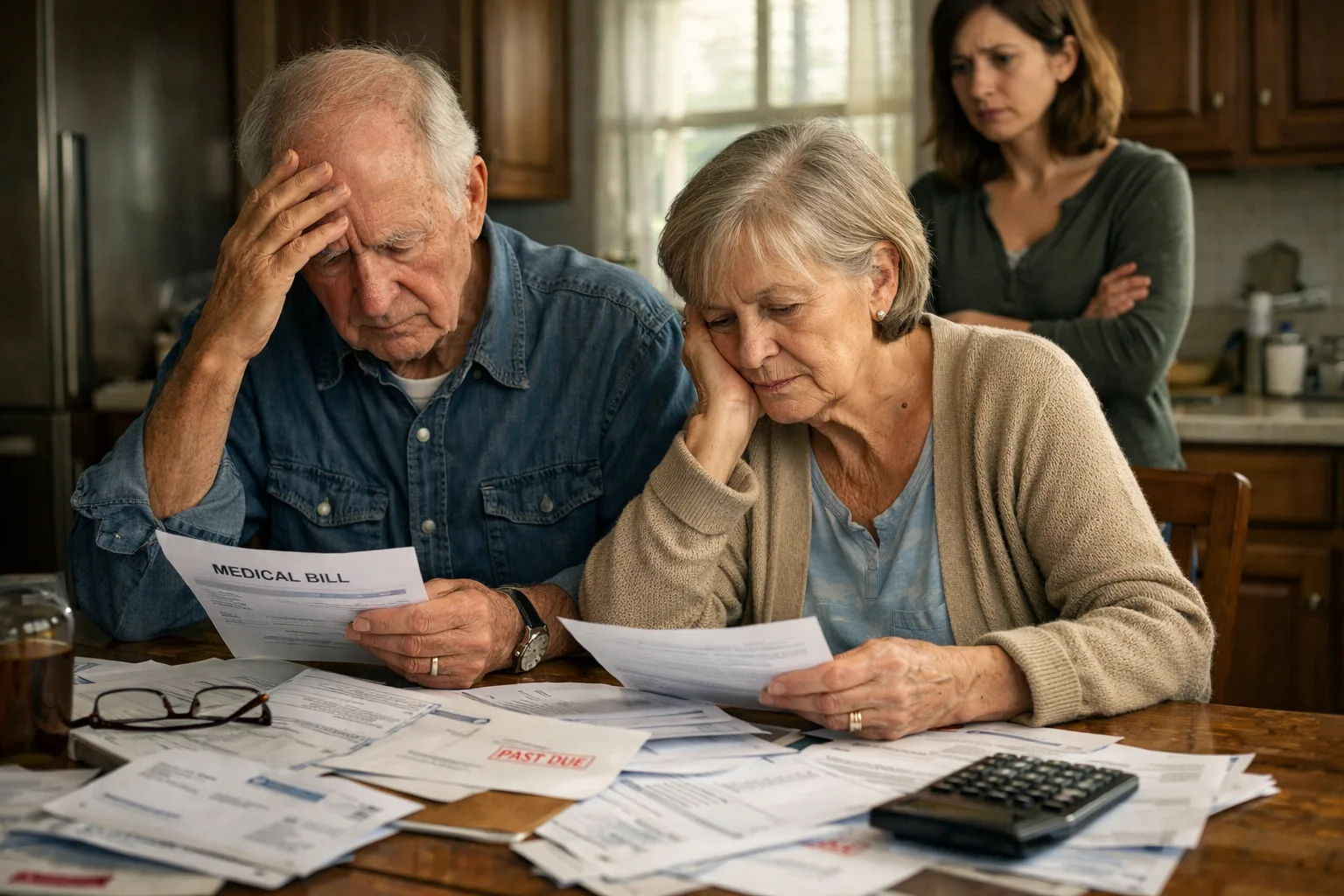

For most families, the reality is blunt. The cost of caring for aging parents or spouses is so high that it is erasing decades of savings, destroying home equity, and in many cases, forcing middle-class households into financial decline.

And according to new research, this is not just a personal finance issue. It is becoming one of the biggest drivers of wealth inequality in America.

The Hidden Force Undermining Generational Wealth

Long-term care includes both medical and non-medical support for individuals who can no longer fully care for themselves. That includes help with basic daily activities like bathing, dressing, eating, or even walking across a room.

Demand is exploding.

More than half of Americans turning 65 today will eventually need some form of long-term care. Roughly one in five will require care for more than five years. At the same time, over 8 million Americans above age 50 already struggle with basic daily activities.

The financial implications are staggering.

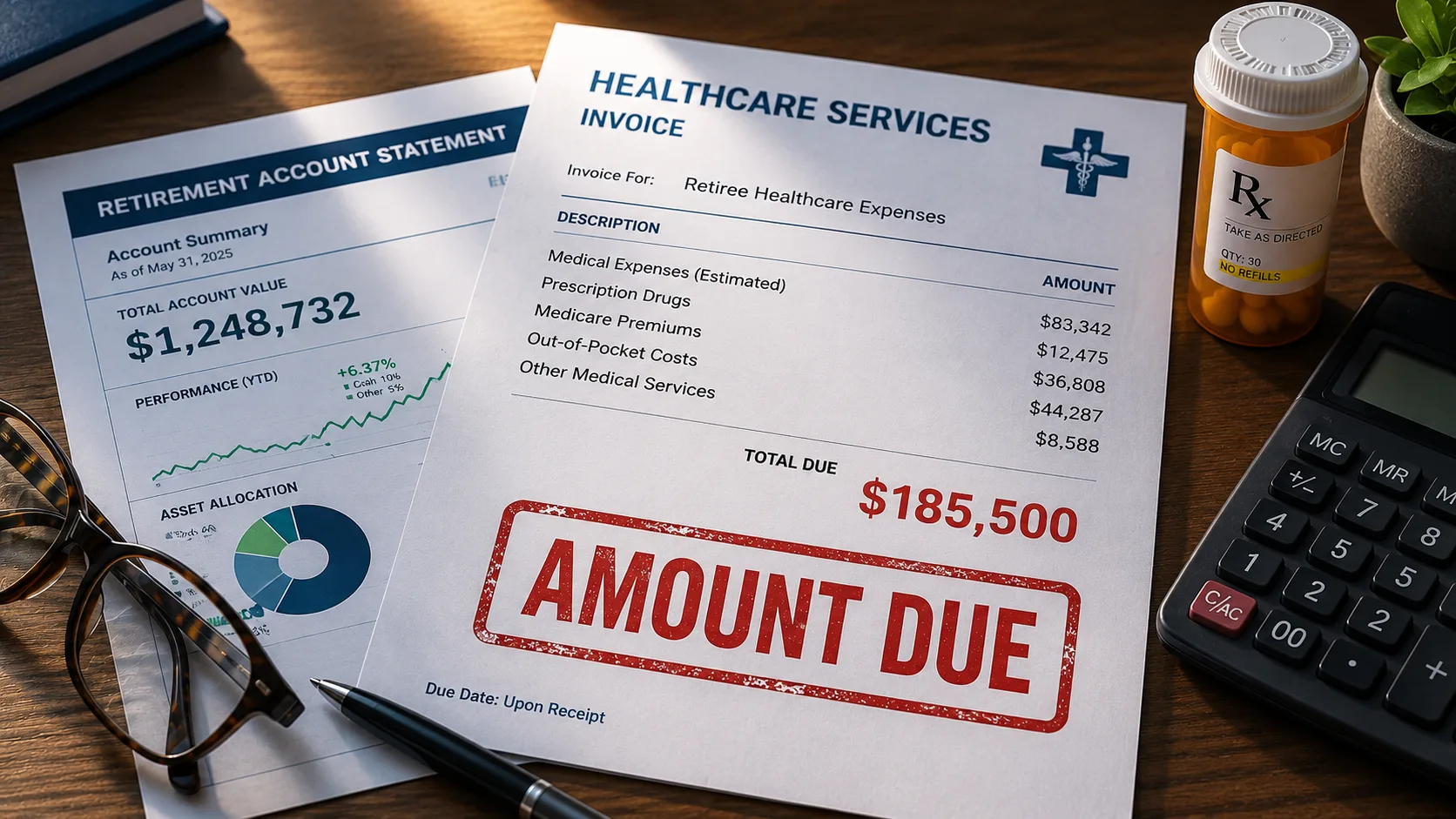

A typical in-home caregiver now costs more than $80,000 per year. Assisted living facilities average over $74,000 annually. A private room in a nursing home can exceed $129,000 per year.

Those numbers are rising fast due to labor shortages, inflation, and increasing demand from an aging population.

For most families, this is not sustainable.

Why the System Is Breaking the Middle Class

The current system puts the burden almost entirely on individuals and families.

Medicare does not cover long-term care. Medicaid does, but only after individuals have essentially spent down their assets to near poverty levels.

That creates a brutal financial reality.

The median household income for Americans over 65 is about $57,000. Meanwhile, retirement savings are alarmingly low. The median retirement savings across all workers is under $1,000 when including those who have saved nothing. Even among those who have saved, the median is only about $40,000.

That gap between income, savings, and care costs is where wealth destruction happens.

Research shows that once long-term care needs begin, middle-class households can lose nearly 60% of their wealth. By contrast, the wealthiest families are largely able to absorb these costs and recover financially.

“Long-term care is both a symptom and a cause of the nation’s deepening wealth divide,” said Jessica Forden of the Roosevelt Institute. “Those at the top of the wealth distribution can absorb long-term-care costs without substantial losses, but for most Americans, the burden of paying for care wipes out decades of savings and home equity.”

In other words, long-term care is accelerating the gap between the rich and everyone else.

The Medicaid Trap Most Americans Fall Into

Medicaid has quietly become the largest payer of long-term care in the United States. But there is a catch.

To qualify, individuals typically must have less than $2,000 in assets.

That means millions of Americans are forced to spend down nearly everything they have before receiving help.

According to research, more than 80% of middle-class seniors who require extended care will eventually end up on Medicaid.

This is one of the biggest structural problems in the system. It effectively penalizes saving while rewarding asset depletion.

For investors and families trying to build generational wealth, that creates a major planning risk.

The $1 Trillion Shadow Economy of Unpaid Care

There is another piece of this crisis that is even less visible.

Most long-term care in America is not provided by professionals. It is handled by family members and friends.

Nearly 60 million Americans act as caregivers, providing an estimated 49.5 billion hours of care each year. If that labor were paid at market rates, it would be worth over $1 trillion annually.

That makes unpaid caregiving one of the largest “invisible industries” in the U.S. economy.

But it comes at a cost.

Caregivers spend an average of $7,200 per year out of pocket. Many cut back on work, turn down promotions, or leave the workforce entirely. That reduces income, slows career growth, and limits retirement savings.

The long-term impact is clear. People caring for aging parents today are putting their own financial futures at risk tomorrow.

As Forden explained, “This ‘free’ care is far from costless. It shifts the bill from aging parents to their adult children by impacting these caregivers’ own capacity for wealth building.”

This creates a ripple effect across generations, weakening financial stability across entire families.

A Growing Care Gap With No Easy Fix

Perhaps the most troubling reality is that many Americans are simply going without care altogether.

Research shows that more than half of older adults who struggle with daily activities receive no assistance. Those without family support are especially vulnerable.

This is not just a financial issue. It is a societal one.

As the population ages, the demand for care will only increase. But the system in place today is not designed to handle it.

That creates serious implications for investors.

The Bottom Line

The idea of a $72 trillion wealth transfer sounds promising. But for many families, that wealth may never make it to the next generation.

Long-term care is quietly becoming one of the biggest financial threats facing American households.

It is draining savings, reshaping retirement plans, and widening the gap between the wealthy and everyone else.

And unless something changes, the cost of aging in America will continue to rise.

For investors and families alike, this is not a future problem.

It is already happening.