CMG stock tumbled nearly 11% after Chipotle Mexican Grill reported disappointing second-quarter earnings and slashed its full-year guidance. Investors are now questioning whether the once-unshakable fast-casual powerhouse has finally hit a wall amid growing economic headwinds.

Q2 2025 Earnings Miss: Consumers Pull Back

In Q2 2025, Chipotle reported revenue of $3.1 billion, a modest 3% increase year-over-year. While top-line growth was roughly in line with expectations, the real damage came from same-store sales, which fell 4%, worse than the anticipated 2.9% decline.

This marked the second straight quarter of negative comps, a troubling sign for a brand that once thrived on robust organic growth. According to Reuters, the decline was largely driven by a 6% drop in foot traffic.

Chipotle’s earnings per share (EPS) landed at $0.33, flat compared to the same quarter last year and in line with analyst expectations. But the broader takeaway was unmistakable: inflation and consumer belt-tightening are finally taking a bite out of Chipotle’s business.

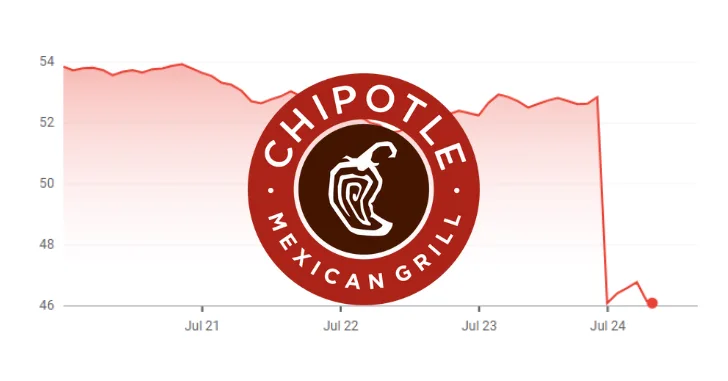

🔻 CMG Stock Nosedives on Downgraded Forecast

The immediate market reaction was brutal. CMG stock plunged more than 10% in after-hours trading, one of its worst single-day drops in recent years. As of July 24, Chipotle’s share price had fallen from $2,280 to around $2,050, erasing billions in market capitalization.

What rattled investors most wasn’t the Q2 miss — it was the guidance cut.

Full-Year Comps Now Expected to Be Flat

Previously, Chipotle projected low single-digit growth in comparable restaurant sales for the full year. Now, the company expects flat comps, suggesting little to no momentum heading into the second half of the year.

“We believe Q2 sales miss and lowered annual guidance is reflective of macro headwinds… rather than executional missteps,” said TD Cowen analyst Andrew Charles, via Reuters.

Why the Slowdown Happened

The earnings report paints a clear picture: consumers are pulling back — particularly lower-income diners and those hit hardest by inflation.

Key Drivers Behind the Weak Performance:

- Shrinking Wallets: Food-at-home prices remain competitive compared to dining out. Many consumers are prioritizing groceries over $10 burritos.

- Limited Pricing Power: Chipotle didn’t raise prices in Q2 and has indicated it will be cautious about future increases, reducing an important lever for margin expansion.

- Marketing Fatigue: The loyalty program and digital ordering infrastructure have matured. They’re no longer providing the same incremental boost to traffic.

- Increased Competition: Fast-casual rivals and cheaper QSRs like Taco Bell, Wendy’s, and Popeyes are actively drawing value-seeking customers.

What Chipotle Is Doing to Turn Things Around

Despite the rocky quarter, Chipotle isn’t sitting idle. Management has outlined a series of initiatives aimed at reviving growth and restoring investor confidence.

1. Menu Innovation

Chipotle launched Adobo Ranch dip, its first new dip in five years, and reintroduced Honey Chicken — both aimed at increasing check sizes and customer excitement.

Early data shows a traffic uptick in June, suggesting the promotions may have helped mitigate some softness.

2. Digital and Loyalty Revamp

Chipotle is increasing its investment in:

- Social media ads

- Push notifications

- Targeted loyalty promotions

The goal? Drive frequency among lapsed and light users. As of Q2, loyalty membership stood at 38 million — a massive database with room to be better monetized.

3. Continued Expansion

Even with traffic pressure, Chipotle opened 61 new locations in Q2 and remains on track for 315–345 new stores in 2025. Expansion is largely focused on suburban areas and new drive-thru “Chipotlanes,” which have shown higher average unit volumes (AUVs).

4. Operational Efficiency

Chipotle is upgrading its kitchen tech and streamlining prep processes. These back-end moves are designed to preserve margins and throughput, even if sales plateau.

Valuation: Still a Premium Stock — for Now

Despite the recent sell-off, CMG stock trades at a forward P/E of 45–47x, significantly above the likes of:

- McDonald’s (MCD) – ~26x

- Starbucks (SBUX) – ~28x

- Domino’s (DPZ) – ~27x

That premium reflects Chipotle’s long-term growth profile and brand strength — but it also leaves the stock vulnerable to downward repricing if comps remain weak through Q3 and Q4.

What Investors Should Watch Next

The next few months are critical. Key areas for investors to monitor include:

July and August Same-Store Sales

Management said comps improved slightly in late June and into July. Third-party transaction data will help confirm if the bounce is sustainable.

New Menu Launches

Chipotle has hinted at more LTOs (limited-time offers) in Q3. These will test the brand’s pricing power and ability to drive urgency.

Inflation and Economic Sentiment

If gas prices or unemployment rise in H2, expect discretionary dining — especially at premium fast-casual chains — to take another hit.

Earnings Revisions

Wall Street is already trimming full-year EPS forecasts. More downward revisions could put pressure on the stock’s valuation multiple.

Is CMG Stock Still a Buy?

CMG stock is facing its biggest operational test since the COVID pandemic. While the brand remains best-in-class in many ways — from supply chain to digital ordering — it’s not immune to macroeconomic gravity.

The current sell-off may offer a buying opportunity if you believe in a H2 recovery and long-term store growth potential. But with comps now projected to be flat and marketing ROI under scrutiny, this is no longer a “set it and forget it” growth story.

For long-term investors, this is a wait-and-watch moment. Keep an eye on comps, inflation, and any signs that Chipotle’s new initiatives are rekindling demand. Until then, the risk/reward on CMG stock has clearly shifted.