The S&P 500 closed Thursday with its 18th record high of the year, fueled by a powerful combination: a stellar U.S. earnings season, booming AI-driven capital spending, and growing expectations that the Federal Reserve will turn more dovish. Volatility has been crushed, with the Cboe Volatility Index (VIX) dipping below 14.5 — its lowest since last December.

But according to a new note from Goldman Sachs researchers Christian Mueller-Glissmann and Andrea Ferrari, history suggests this type of quiet often ends with turbulence.

The “Unfriendly Asymmetry” in Today’s Market

Goldman’s warning centers on a structural imbalance they call a “less friendly” asymmetry.

- Big rallies are less likely in low-volatility environments because the largest upside moves usually occur during economic recoveries, not at record highs.

- The odds of a sharp drop are rising, fueled by expensive valuations, slowing growth indicators, and potential inflationary shocks from higher tariffs.

Recent strength in the S&P 500, they note, has been valuation-driven rather than earnings-driven. Credit spreads have tightened significantly, suggesting investors may be underestimating economic damage from trade policies — particularly increased tariffs.

Tariffs, Inflation, and the Fed’s Dilemma

The recent producer price index surprise reinforced fears that tariff-related cost pressures could delay or reduce expected Fed rate cuts. Meanwhile, geopolitical tensions remain a wildcard.

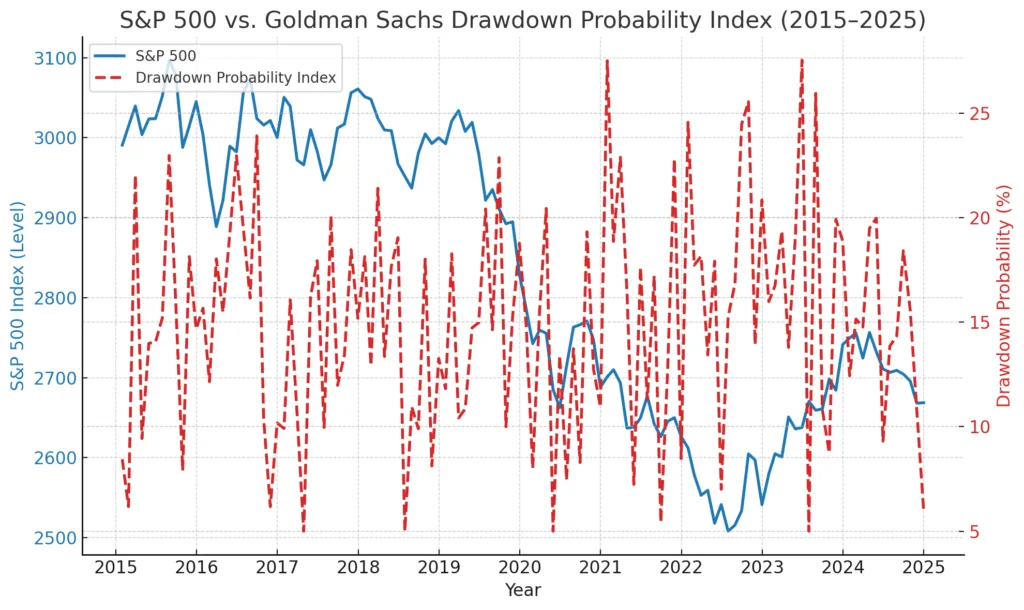

Goldman’s proprietary S&P 500 drawdown probability index has climbed to levels last seen during President Trump’s April “Liberation Day” tariff announcement. That spike in risk is compounded by weaker labor market data and slowing business cycle momentum.

Their economists expect U.S. growth to remain soft in the second half of the year. While this might justify more Fed easing, any rate cuts are likely to arrive alongside higher volatility, not in a smooth, rally-friendly environment.

Portfolio Positioning: Caution Over Conviction

Goldman’s current tactical asset allocation:

- Overweight cash

- Neutral on equities, credit, and bonds

- Underweight commodities

They recommend cheap put spreads as a cost-effective hedge against equity declines. A put spread involves buying one put option while selling another at a lower strike price, lowering the cost of protection while capping potential profit.

For the next three months, Goldman sees value in selective downside hedges across emerging market and European equities — specifically Brazil’s Bovespa, India’s Nifty 50, and China’s CSI 300. On the upside, they note that calls on the S&P 500 equal-weight index could benefit if gains broaden beyond mega-cap tech stocks.

Market Snapshot

| Asset/Class | Last Price | 5D Change | 1M Change | YTD Change | 1Y Change |

|---|---|---|---|---|---|

| S&P 500 | 6,468.54 | +2.03% | +2.72% | +9.98% | +16.69% |

| Nasdaq | 21,710.67 | +2.20% | +3.95% | +12.43% | +23.39% |

| 10-Yr U.S. Treasury Yield | 4.29% | +0.40bps | -13.30bps | -28.60bps | +40.50bps |

| Gold (futures) | $3,390.50 | -1.96% | +1.05% | +28.46% | +33.16% |

| Oil (WTI) | $63.52 | +0.27% | -3.80% | -11.62% | -15.86% |

Investor Takeaways

- Beware of complacency — historically, extended low-volatility periods often end with sharp drawdowns.

- Valuation-driven rallies are inherently fragile; they offer less cushion when macro shocks hit.

- Tariff-driven inflation could trap the Fed between fighting price pressures and supporting growth, creating an unstable policy backdrop.

- Options-based hedges can protect portfolios at relatively low cost, especially via put spreads or targeted emerging market trades.

- Watch for breadth in the rally — gains spreading beyond mega-cap tech could shift leadership dynamics in the market.

Bottom line for investors:

Goldman’s message isn’t to abandon stocks — it’s to prepare for a regime shift. The next few months could bring higher volatility and asymmetric downside risk, even if earnings remain strong. Strategic hedges, diversified exposures, and disciplined risk management will be key to navigating the transition from calm to choppier waters.