Americans are obsessing over inflation, tariffs, and whether the stock market is overvalued. Many are missing a slower-moving financial threat that may be even more dangerous to their long-term wealth: living far longer than their retirement plan can support.

That risk is becoming far more expensive.

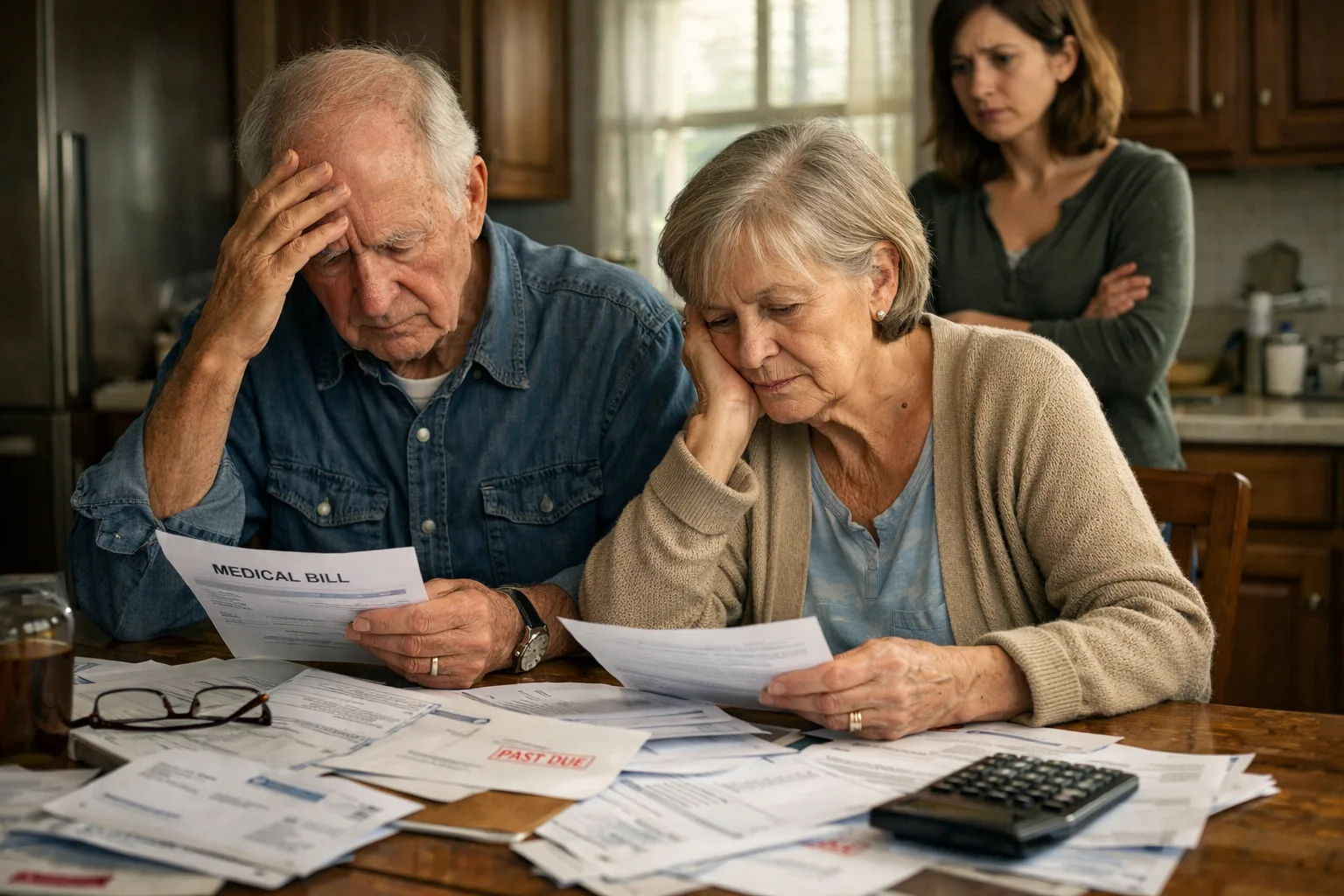

According to new research from the TIAA Institute, only one in three Americans can correctly estimate how long a typical 65-year-old will live. That misunderstanding is quietly shaping bad financial decisions. People who underestimate longevity save less, invest differently, and often assume retirement is a shorter phase of life than reality suggests.

The actual numbers are far more sobering.

A 65-year-old man today has an average life expectancy of 84. A woman has an average life expectancy of 87. There is also a 30% chance a 65-year-old man reaches age 90 and a 40% chance a woman does the same.

That means millions of Americans are unknowingly building retirement plans designed for a sprint while reality may require marathon-level capital.

And that has massive implications for investors, financial advisors, healthcare companies, insurance firms, dividend stocks, annuities, retirement housing operators, and anyone trying to preserve wealth over multiple decades.

The retirement crisis most investors talk about centers around inflation.

The bigger issue may be time itself.

What Actually Happened: America’s Retirement Math Is Breaking

Northwestern Mutual recently found Americans believe they need roughly $1.46 million to retire comfortably.

Meanwhile, the National Institute on Retirement Security found the median retirement savings balance for American workers sits at just $955.

Yes, $955.

That gap alone tells you retirement planning in America is deeply broken.

Then add another major pressure point: pensions have largely disappeared from the private sector. Workers now shoulder far more responsibility through 401(k)s, IRAs, brokerage accounts, and personal savings.

Then there is Social Security Administration risk.

The agency’s trust funds are projected to face insolvency pressure by 2032 unless lawmakers intervene, which could trigger automatic benefit reductions.

That matters because millions of retirees rely heavily on Social Security as foundational income.

The old retirement formula used to be straightforward:

- Work for 40 years

- Retire at 65

- Collect pension income

- Rely on Social Security

- Live another 10 to 15 years

That formula is largely gone.

Today’s version looks much different:

- Work for 40 years

- Retire at 65

- Self-fund retirement

- Manage healthcare inflation

- Navigate volatile markets

- Potentially fund 25 to 35 years of living expenses

That is a radically different financial challenge.

And many households still have not adjusted.

Longevity Is Creating a New Asset Allocation Problem

Most media coverage frames longer life expectancy as a personal finance story.

That is too narrow.

This is becoming a major capital markets story.

Why?

Because a longer retirement changes how money behaves.

If retirement lasts 30 years instead of 12 years, investors cannot simply shift entirely into low-yield assets and hope for the best.

A retiree who moves everything into cash or bonds too early may protect principal in the short term but create a long-term income problem later.

At the same time, staying too aggressive in equities can expose retirees to sequence-of-returns risk.

This happens when market declines hit early in retirement while investors are simultaneously making withdrawals.

A major bear market during the first five years of retirement can permanently damage portfolio sustainability.

This creates a balancing act Wall Street is increasingly trying to solve.

That is one reason target-date funds, structured income products, annuities, dividend ETFs, and alternative income products continue attracting attention.

Firms like BlackRock, Vanguard, and Charles Schwab are aggressively expanding retirement income offerings because they understand longevity is becoming a massive economic theme.

Insurance giants like Allianz are also benefiting from increased demand for guaranteed income products as retirees become more fearful of running out of money.

And that fear is very real.

Allianz found 67% of Americans are more afraid of outliving their savings than dying.

That should tell investors everything they need to know.

Why This Matters for Investors

Longer retirements likely mean continued inflows into retirement-focused investment products.

Expect growth in:

- Dividend ETFs

- Target-date funds

- Annuities

- Income-focused REITs

- Healthcare ETFs

- Long-term care investments

- Wealth preservation strategies

This may also strengthen demand for lower-volatility equities.

Companies with predictable cash flow, stable dividends, and recession resilience could remain attractive as America ages.

Think utilities, healthcare infrastructure, consumer staples, and certain insurers.

Rates

Higher interest rates temporarily helped retirees by improving yields on savings products, CDs, and bonds.

But rate volatility remains dangerous.

If rates fall sharply in future years, retirees chasing income may be forced back into riskier assets.

That could create major reallocations across bonds, dividend stocks, and alternative income products.

Watch the Federal Reserve closely.

Its policy decisions will directly impact retirement income strategies.

Healthcare

This may be one of the biggest winners.

Longer lives often mean higher healthcare spending.

That could benefit:

- UnitedHealth Group

- Humana

- CVS Health

- Senior housing REITs

- Medical device makers

- Home healthcare providers

The longevity economy could become one of the largest investment themes of the next two decades.

Housing

Senior housing demand could rise significantly.

Companies tied to retirement communities, assisted living, and aging-in-place technologies may benefit as older Americans seek lower-maintenance living arrangements.

The “Retirement Duration Multiplier”

Here’s the framework investors should remember:

Longer life expectancy creates exponential retirement costs.

Call this the Retirement Duration Multiplier:

Longer lifespan → More healthcare costs → More inflation exposure → More withdrawal years → Higher portfolio pressure

This compounds quickly.

A retiree spending $80,000 annually for 15 years needs far less capital than someone spending $80,000 annually for 30 years while facing healthcare inflation.

That second scenario can destroy underfunded portfolios.

Investors who fail to plan for this multiplier may find themselves forced into poor decisions later.

The math becomes brutal fast.

Longer Lives Are Also Creating Investment Opportunities

Most retirement coverage focuses entirely on fear.

That misses the opportunity side.

Longer life expectancy creates entirely new markets.

The companies that help Americans live longer, healthier, and more financially secure lives could see massive tailwinds.

This includes:

- Wealth management firms

- Financial planning technology platforms

- Insurance companies

- Healthcare innovators

- Senior housing operators

- Home care providers

- Medical robotics firms

- Preventative healthcare companies

This is where investors should think bigger.

America’s aging population is often discussed as a burden.

For investors positioned correctly, it may become one of the most predictable long-term demographic trends in the market.