Retirement is often described as the “finish line” of a long financial race, but for many investors, crossing that line is where the most complex hurdles actually begin. While the accumulation phase is relatively straightforward: save early, diversify often: the distribution phase is a tactical minefield of tax brackets, Medicare surcharges, and shifting regulatory deadlines.

As we move into June 2026, the landscape for retirees has shifted significantly. With the Required Minimum Distribution (RMD) age now firmly set at 73 for most and new tax deductions coming into play, the “set it and forget it” withdrawal strategy is no longer a viable option. For those managing their own portfolios, avoiding common tactical errors is the difference between a comfortable retirement and one plagued by “tax bombs” and avoidable surcharges.

The Pitfalls of the Conventional Withdrawal Sequence

For decades, the standard advice for retirees was simple: spend your taxable brokerage accounts first, then move to your tax-deferred IRAs and 401(k)s, and finally touch your tax-free Roth accounts. This strategy was designed to maximize the time your money spent growing inside tax-advantaged shells. However, in the 2026 tax environment, this rigid adherence to “taxable-first” can lead to a massive tax spike in later years.

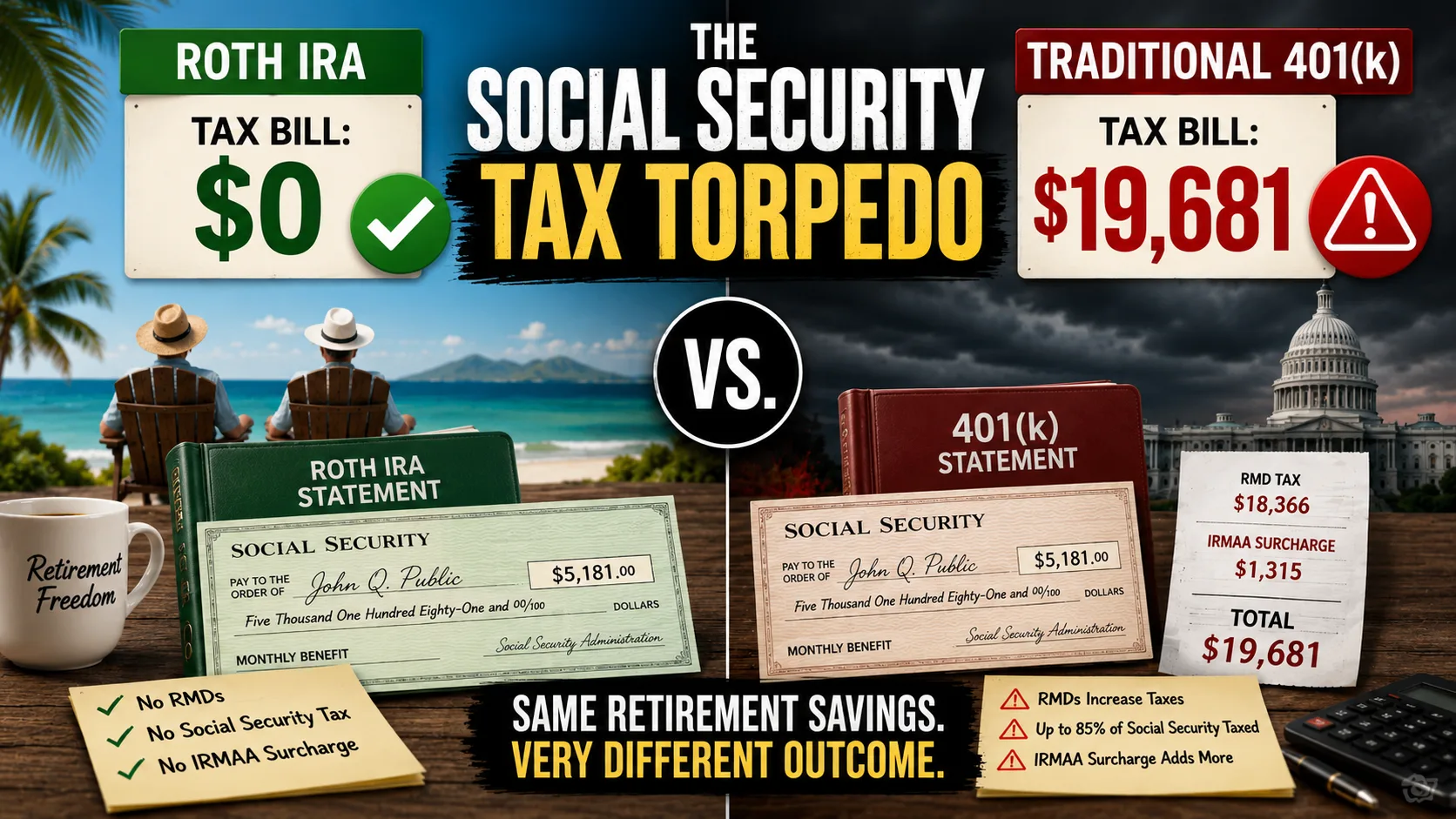

When investors ignore their tax-deferred accounts for the first decade of retirement, they allow those balances to balloon. By the time they hit the age of 73: the current RMD starting age: the mandatory distributions can be so large that they push the retiree into a much higher tax bracket than they were in during their working years. This “tax bomb” is often accompanied by a significant increase in Medicare premiums.

A more modern approach involves “bracket topping”: taking enough from your IRA to fill up your current low tax bracket, even if you don’t technically need the money for living expenses. This levels out your lifetime tax bill rather than back-loading it into your 80s.

Miscalculating the Safe Withdrawal Rate

The most persistent ghost in the retirement planning room is the “4% Rule.” While it served as a useful benchmark for decades, the economic realities of 2026 have called its universal applicability into question. With higher volatility in global markets and the lingering effects of historical inflation, blindly withdrawing 4% of your starting balance (adjusted for inflation) can lead to premature portfolio depletion.

Investors who fail to adjust their withdrawal rates based on market performance: known as “Sequence of Returns Risk”: run the risk of selling assets when they are down, locking in losses that can never be recovered. As we have explored previously, many experts now argue that The 4% Rule is Dead, necessitating a more dynamic approach that adjusts based on annual market returns and personal longevity expectations.

Squandering the “Gap Years” Opportunity

One of the most frequent mistakes made by early retirees (those between ages 60 and 72) is failing to utilize their “Gap Years.” These are the years after you stop receiving a paycheck but before you are forced to take RMDs or start Social Security. In 2026, these years represent a golden window for Roth conversions.

By converting portions of a Traditional IRA to a Roth IRA during these low-income years, you pay taxes at today’s potentially lower rates. This not only builds a tax-free bucket for the future but also reduces the total balance subject to RMDs later on. Furthermore, because Roth IRAs do not have RMDs for the original owner, this strategy offers unparalleled flexibility in old age. If you skip these years without a conversion strategy, you are essentially leaving a tax-efficiency tool on the table that cannot be reclaimed once RMDs begin.

Falling Off the IRMAA Cliff

Perhaps the most frustrating “stealth tax” in retirement is the Income-Related Monthly Adjustment Amount, or IRMAA. These are surcharges added to Medicare Part B and Part D premiums for individuals whose income exceeds certain thresholds. What many retirees miss is the “two-year look-back” rule. Your 2026 Medicare premiums are determined by the Adjusted Gross Income (AGI) you reported on your 2024 tax return.

Crossing an IRMAA threshold by even a single dollar can result in thousands of dollars in extra premiums over the course of a year. For example, a large, one-time IRA withdrawal to buy a vacation home or a significant capital gain from a stock sale in 2024 can come back to haunt your 2026 budget. To avoid this cliff, retirees must proactively manage their MAGI (Modified Adjusted Gross Income) to stay just below the tiered thresholds.

Overlooking the 2026 Senior Tax Benefits

The tax code provides several “carrots” for older investors that often go unnoticed. For 2026, the additional standard deduction for those aged 65 and older has become a powerful tool. When combined with the regular standard deduction, a married couple both over 65 can effectively shield a significant amount of income: often cited as the “senior deduction” benefit of over $6,000 in additional tax-free space compared to younger filers.

Failing to “fill” this 0% tax bracket with ordinary income like IRA withdrawals is a missed opportunity. If your fixed income from Social Security or pensions doesn’t reach this threshold, you are effectively letting tax-free withdrawal space go to waste.

Additionally, for those who are charitably inclined, the Qualified Charitable Distribution (QCD) remains the single most efficient way to give. If you are 70½ or older, you can transfer up to $111,000 (the 2026 limit) directly from your IRA to a qualified charity. This amount counts toward your RMD but is not included in your AGI, which can help you stay below the aforementioned IRMAA thresholds.

The Double-RMD Blunder in the First Year

The SECURE Act 2.0 shifted the RMD age to 73, but it didn’t change the peculiar rule regarding the first year’s distribution. If you turn 73 in 2026, you have the option to delay your first RMD until April 1, 2027. On the surface, this looks like a win: you get to keep your money growing for another few months.

However, this is often a trap. If you delay your first RMD into 2027, you must still take your second RMD by December 31, 2027. This results in two RMDs being taxed in a single calendar year. This “double distribution” can spike your income, push you into a higher tax bracket, and trigger massive IRMAA surcharges two years down the line. In almost all cases, it is mathematically superior to take that first distribution by December 31st of the year you turn 73 to keep your income levels smooth.

Neglecting Portfolio Protection Against Inflation

Finally, many withdrawal strategies fail because they assume a static economic environment. While your withdrawal rate might be calculated perfectly, your portfolio’s underlying assets must still combat the eroding effects of inflation. Relying too heavily on fixed-income assets in early retirement can leave you vulnerable.

Integrating inflation-sensitive assets is critical. For instance, Protecting Your Retirement from Inflation often requires a mix of equities and hard assets. Real Estate Investment Trusts (REITs) are a popular choice for this purpose, as they often provide a yield that keeps pace with rising costs. Investors looking for income and growth in 2026 might consider reviewing the 10 Best REITs currently leading the market.

Navigating the Road Ahead

Managing a retirement withdrawal strategy is not a one-time event; it is an annual exercise in tactical navigation. The transition from age 60 to 73 involves a series of critical decision points: from the “gap years” of Roth conversions to the eventual onset of RMDs and IRMAA considerations.

By avoiding the traps of rigid withdrawal sequences and being proactive about 2026’s specific tax benefits like QCDs and the expanded senior deduction, investors can ensure that their retirement savings last as long as they do. The goal is not just to have enough money to retire, but to have enough strategy to keep it.