For many Americans, retirement represents decades of hard work, disciplined saving, and careful financial planning. Unfortunately, a growing wave of sophisticated scams is threatening that financial security, and the losses are reaching record levels.

According to newly released FBI data, Americans aged 60 and older reported losing an astonishing $7.7 billion to internet fraud in 2025. That figure marks a significant increase from the previous year and highlights a troubling reality: scammers are increasingly targeting retirees, often with devastating financial consequences.

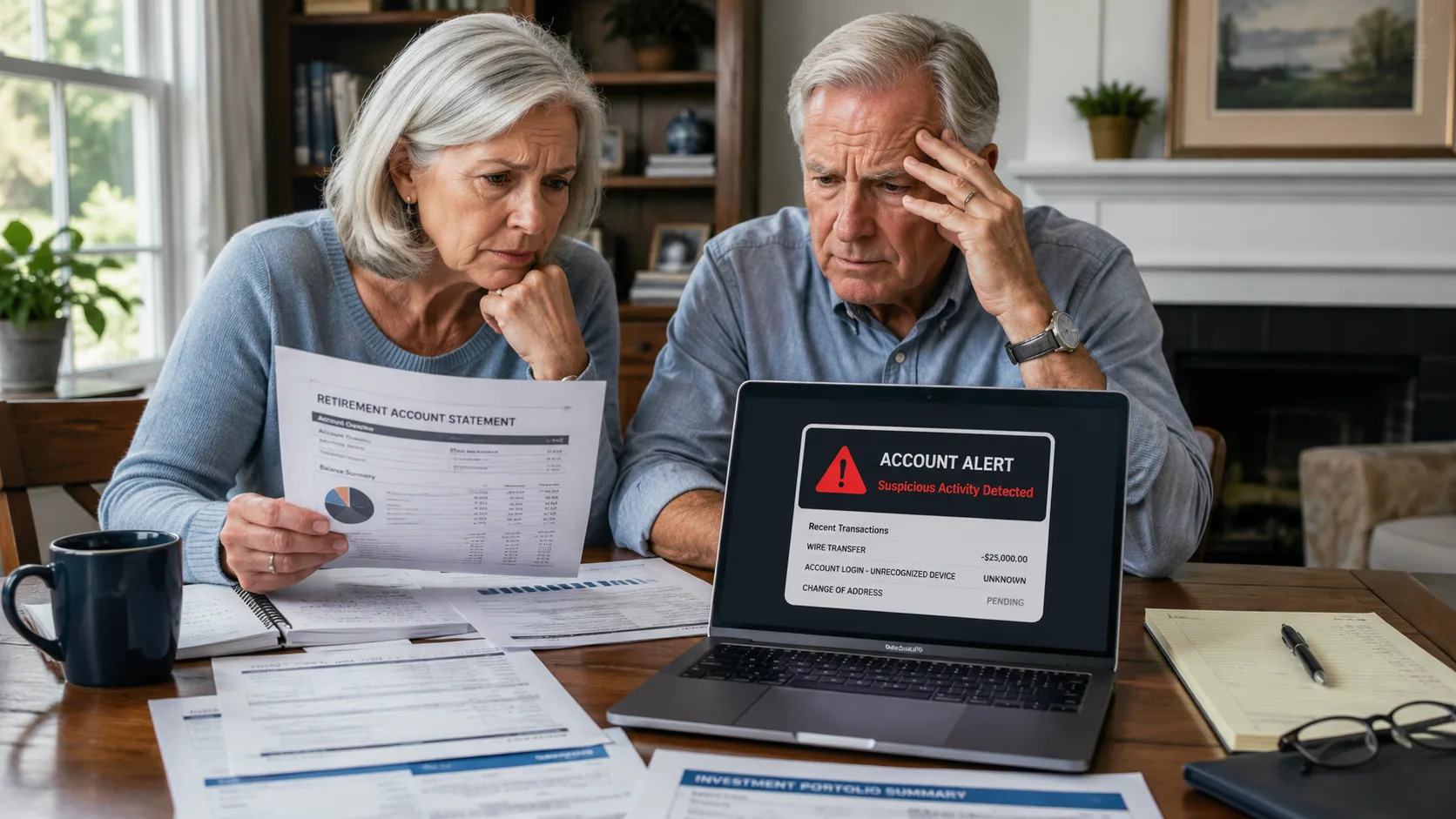

For investors and retirees alike, protecting savings is no longer just about managing market risk. It is also about recognizing the fraud schemes that continue to drain billions from older Americans every year.

Why Older Americans Are Becoming Prime Targets

Internet fraud has surged across virtually every age group, but retirees are bearing the largest financial burden.

The FBI received more than 201,000 complaints from Americans over age 60 during 2025, representing a 37% increase from the previous year. While younger adults also reported substantial losses, seniors accounted for a disproportionate share of the financial damage.

Several factors may explain why criminals increasingly target retirees. Many older Americans have accumulated larger savings balances, own valuable assets, and maintain multiple financial accounts. In addition, retirement portfolios often contain substantial cash reserves that can be quickly accessed and transferred.

Once funds are stolen, recovering them can be difficult or impossible, particularly when scammers use cryptocurrency, wire transfers, or overseas accounts.

Here are the five scam categories that caused the most damage to retirees in 2025.

1. Investment Scams Remain the Biggest Financial Threat

Investment fraud continues to be the most costly scam facing older Americans.

These schemes often promise exclusive opportunities, guaranteed returns, insider information, or access to high-performing investments. Fraudsters frequently create professional-looking websites, fake account statements, and convincing sales presentations designed to mimic legitimate investment firms.

Many victims believe they are investing in real estate projects, private placements, cryptocurrency ventures, or high-yield income opportunities.

According to FBI data, retirees lost more than $3.5 billion to investment scams in 2025 alone.

That total makes investment fraud by far the most expensive category reported by older Americans.

Why Investors Fall Victim

Many investment scams exploit emotions such as fear of missing out, concerns about inflation, or the desire to generate higher retirement income. Criminals understand these concerns and tailor their pitches accordingly.

Common warning signs include:

- Guaranteed returns

- Pressure to invest immediately

- Claims of exclusive access

- Unregistered investment offerings

- Requests for wire transfers or cryptocurrency payments

If an opportunity sounds too good to be true, it usually is.

2. Tech Support Scams Continue to Drain Retirement Savings

Tech support scams remain one of the most successful fraud tactics used against seniors.

The scam often begins with a pop-up warning, phone call, email, or text message claiming that a computer has been infected with malware or compromised by hackers. Victims are instructed to contact a support number or allow a technician remote access to their device.

The “technician” is actually a scammer.

Once access is granted, criminals may steal passwords, install malicious software, gain access to banking accounts, or persuade victims to send money to fix problems that never existed.

Older Americans reported losses exceeding $1.04 billion from tech support and customer service scams during 2025.

Red Flags to Watch For

Legitimate technology companies do not typically:

- Contact customers unexpectedly about viruses

- Request remote access without a support request

- Demand payment through gift cards

- Threaten immediate account shutdown

When in doubt, contact the company directly using its official website or customer service number.

3. Romance Scams Are Costing Victims Nearly $1 Billion

Not all scams rely on technology. Some rely on emotional manipulation.

Romance scams occur when criminals build online relationships through social media platforms, dating websites, or messaging apps. Over time, they establish trust and emotional connections before introducing financial emergencies.

Victims may be told that a loved one needs medical treatment, travel expenses must be covered, or an unexpected crisis requires immediate assistance.

By the time money requests begin, victims often believe they are helping someone they genuinely care about.

The FBI reports that older Americans lost approximately $929 million to romance and confidence scams in 2025.

Why Romance Scams Are So Dangerous

Unlike many fraud schemes that involve a single transaction, romance scams often unfold over months or even years.

Victims may send multiple payments, liquidate investments, or withdraw retirement savings before realizing they have been deceived.

The emotional impact can be just as severe as the financial loss.

4. Identity Theft Can Create Long-Term Financial Damage

Identity theft remains a major concern for retirees.

Criminals use stolen personal information to open credit accounts, access existing financial accounts, file fraudulent tax returns, or commit other forms of financial fraud.

The challenge is that many victims do not immediately realize their information has been compromised.

By the time suspicious activity is discovered, significant damage may already have occurred.

Older Americans reported more than $185 million in losses tied directly to identity theft in 2025.

Recovery Can Take Months

Identity theft often creates challenges beyond the initial financial loss.

Victims may spend months:

- Closing fraudulent accounts

- Rebuilding damaged credit

- Replacing identification documents

- Disputing unauthorized transactions

Regularly monitoring financial accounts and credit reports can help identify suspicious activity before losses escalate.

5. Government Impersonation Scams Continue to Fool Thousands

Government impersonation scams have become increasingly sophisticated.

Fraudsters pretend to represent agencies such as the IRS, Social Security Administration, Medicare, or law enforcement. They contact victims claiming taxes are owed, benefits are at risk, or legal action is imminent.

The goal is simple: create panic and urgency.

Victims are pressured to act immediately before they have time to verify the claims.

According to FBI data, seniors lost more than $413 million to government impersonation scams in 2025.

One Important Rule

Government agencies generally do not:

- Demand immediate payment

- Request gift card purchases

- Require cryptocurrency transfers

- Threaten arrest over the phone

Any communication making those demands should be treated with extreme skepticism.

The Average Victim Lost More Than $38,000

Perhaps the most alarming statistic in the FBI report is the average loss per victim.

Among Americans over age 60 who reported fraud, the average financial loss reached approximately $38,500.

Even more concerning, more than 12,000 victims reported losing over $100,000.

For many retirees, those losses represent years of savings, emergency reserves, or income intended to support decades of retirement.

These States Reported the Highest Losses

The largest financial losses occurred in states with substantial retiree populations and significant concentrations of wealth.

The five hardest-hit states were:

- California: $1.40 billion

- Florida: $709.8 million

- Texas: $678.6 million

- New York: $408.7 million

- Arizona: $344.0 million

While population size plays a role, these figures also suggest scammers may focus heavily on regions with higher concentrations of affluent retirees.

How Retirees Can Protect Their Savings

While no strategy can eliminate risk entirely, several simple precautions can significantly reduce the likelihood of becoming a victim.

Experts recommend:

- Never sending money based on pressure or urgency

- Verifying unexpected requests independently

- Using multi-factor authentication on financial accounts

- Monitoring bank and investment accounts regularly

- Freezing credit when appropriate

- Consulting trusted family members or financial advisors before large transactions

- Reporting suspicious activity immediately

The faster potential fraud is identified, the greater the chances of limiting financial damage.

Why Scam Awareness May Be the Most Important Retirement Strategy

Most retirement planning focuses on investing, budgeting, taxes, and withdrawal strategies. Yet the FBI’s latest data highlights another critical risk that deserves equal attention.

Scammers stole billions from older Americans in 2025, and the tactics continue to evolve every year.

Understanding how these schemes work may be one of the most effective ways retirees can protect the savings they’ve spent a lifetime building.

As fraudsters become increasingly sophisticated, vigilance is no longer optional. It is an essential part of preserving long-term financial security in retirement.