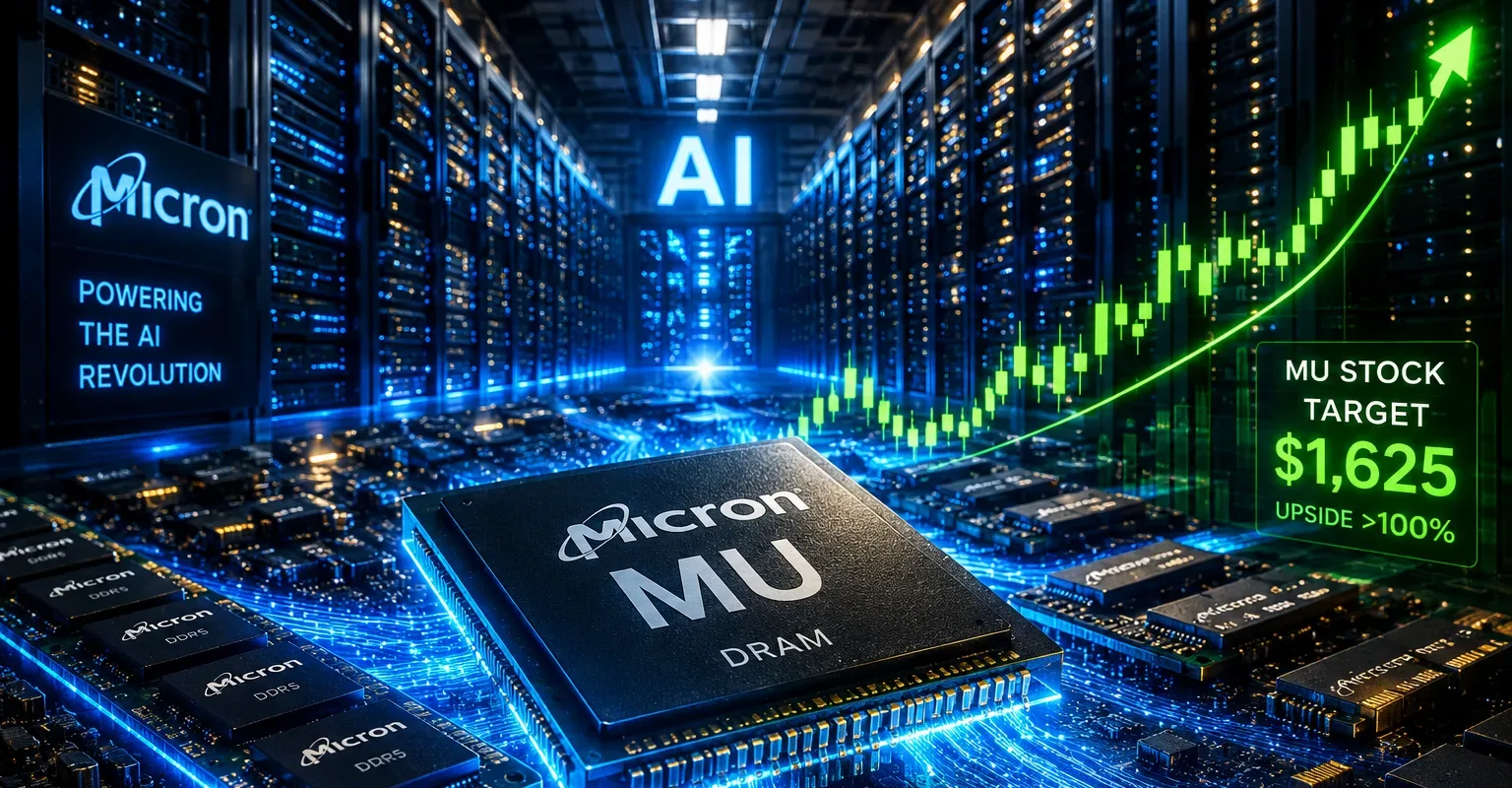

Shares of Micron Technology surged Tuesday after analysts at UBS issued one of the most aggressive bullish calls Wall Street has seen on the semiconductor giant in years, reigniting debate over whether MU stock could become one of the defining AI infrastructure winners of the decade.

The bank raised its price target on Micron from $535 to $1,625, implying more than 100% upside from current levels and signaling growing confidence that the memory-chip industry is undergoing a structural transformation driven by artificial intelligence demand.

MU stock climbed sharply in premarket trading following the announcement, as investors rushed back into semiconductor names tied to the AI buildout.

The rally reflects a larger shift happening across markets right now.

For much of the last two decades, memory-chip companies were viewed as deeply cyclical businesses. Investors often treated them as boom-and-bust commodity producers vulnerable to pricing collapses, oversupply, and brutal downturns.

UBS now believes that narrative may be breaking down.

Why MU Stock Is Suddenly Back in Focus

The key catalyst behind the bullish call centers on long-term supply agreements.

According to UBS analyst Timothy Arcuri, major cloud computing providers and AI infrastructure companies are increasingly locking in memory supply years in advance. That changes the economics of the industry dramatically.

Instead of relying entirely on volatile spot-market pricing, companies like Micron are now securing multi-year contracts that provide:

- Guaranteed demand visibility

- Fixed or semi-fixed pricing

- More stable revenue streams

- Reduced earnings volatility

- Stronger long-term capital planning

UBS estimates that roughly 30% of global DDR memory volumes could soon fall under these types of agreements.

That matters because memory chips are no longer just interchangeable commodity products.

They are becoming critical infrastructure for AI systems.

The AI Arms Race Is Fueling Memory Demand

The artificial intelligence boom has created an enormous need for high-bandwidth memory, advanced DRAM, and NAND storage products.

Every major AI data center requires massive amounts of memory to train and run large language models.

Companies like Nvidia, Microsoft, Amazon, Meta, and Google are all spending aggressively to expand AI infrastructure.

That spending wave is increasingly benefiting memory suppliers.

UBS noted that hyperscale cloud providers have already secured between 60% and 70% of industry-wide server DDR5 supply through enhanced long-term contracts.

That effectively gives Micron a guaranteed customer base for some of its highest-margin products.

This is one reason why Wall Street is beginning to rethink MU stock entirely.

UBS Makes the Nvidia Comparison

One of the most eye-catching parts of the UBS note was the comparison to Nvidia.

Arcuri argued there is “no reason why MU should trade a whole lot differently than NVDA in terms of P/E.”

That is an extraordinary statement given Nvidia’s premium valuation and dominant AI positioning.

Historically, Micron traded at much lower valuation multiples because investors feared unpredictable earnings swings tied to memory pricing cycles.

But if AI demand creates sustained shortages and long-term supply agreements smooth out volatility, MU stock could begin receiving a much higher multiple from investors.

That appears to be the core thesis behind UBS’s massive price target increase.

The Hidden Story Investors May Be Missing

Most investors still think about AI through the lens of GPUs.

That may be a mistake.

The real AI bottleneck increasingly may become memory capacity and bandwidth.

As AI models grow larger and more complex, they require exponentially greater amounts of high-performance memory to function efficiently.

Without advanced memory systems, even the most powerful GPUs become constrained.

This is where Micron could emerge as one of the quiet winners of the AI era.

The company sits in a strategically important position inside the semiconductor ecosystem.

And unlike some AI names already trading at historically extreme valuations, MU stock still carries the legacy perception of a cyclical hardware business.

If Wall Street fully reprices Micron as a core AI infrastructure provider instead, the stock’s long-term upside could look very different than what many investors currently expect.

Mizuho Also Stays Bullish on MU Stock

UBS was not alone in expressing optimism.

Mizuho Financial Group reiterated its Outperform rating on Micron and maintained an $800 price target while continuing to classify the company as a Top Pick.

Analyst Vijay Rakesh emphasized that AI-driven demand trends still appear to be in the early stages.

“We believe there’s no clear line of sight on when the supply-demand imbalance could end as demand durability sees secular long-term tailwinds with DRAM/NAND as key AI enablers,” Rakesh wrote.

That language matters.

It suggests some analysts believe the industry may not experience the traditional oversupply collapse investors became accustomed to in previous cycles.

Instead, AI infrastructure demand could create a prolonged period of elevated pricing power.

Micron’s Earnings Outlook Just Changed Dramatically

UBS also significantly raised its earnings forecasts for Micron through 2029.

The firm now projects:

| Year | Previous EPS Forecast | New EPS Forecast |

|---|---|---|

| 2027 | $133 | $155 |

| 2028 | $122 | $167 |

| 2029 | $77 | $117 |

Perhaps more importantly, UBS forecasts Micron could generate more than $400 billion in free cash flow during that stretch.

Even in a moderate downturn scenario for memory markets in 2029, the bank still expects earnings per share to remain comfortably above $100.

That would represent a major departure from the violent earnings collapses memory companies historically suffered during down cycles.

What Could Go Wrong for MU Stock?

Despite the bullish momentum, investors should understand the risks.

The semiconductor industry remains highly competitive and capital intensive.

Potential risks include:

- A slowdown in AI spending

- Overcapacity returning to memory markets

- Geopolitical tensions involving Taiwan or China

- Export restrictions affecting semiconductor sales

- Economic slowdowns reducing enterprise cloud spending

- Aggressive competition from rivals like Samsung Electronics and SK Hynix

There is also the possibility that current AI demand enthusiasm becomes overheated.

Markets have already seen massive rallies across AI-related stocks, and expectations are becoming increasingly aggressive.

If hyperscaler spending slows even modestly, valuations across the semiconductor sector could come under pressure quickly.

Why This Matters Beyond Micron

The bigger story here may extend beyond MU stock itself.

Wall Street increasingly appears willing to reward companies that provide the underlying infrastructure powering artificial intelligence.

For years, investors focused mainly on software platforms and cloud services.

Now, the market is shifting toward the physical hardware ecosystem required to support AI expansion.

That includes:

- GPUs

- Advanced memory

- Networking chips

- Data-center infrastructure

- Power systems

- Cooling technologies

Micron sits directly inside that supply chain.

And if the AI boom continues expanding globally, demand for advanced memory products could remain elevated far longer than many investors anticipated.

Investor Takeaway on MU Stock

MU stock is no longer simply trading as a traditional memory-chip manufacturer.

Wall Street is increasingly beginning to value Micron as an AI infrastructure company.

That distinction could matter enormously over the next several years.

UBS’s aggressive price target may prove overly optimistic. But the underlying thesis reflects a real shift happening across the semiconductor industry.

Long-term contracts, hyperscaler demand, and AI infrastructure expansion are changing how investors think about memory companies.

If those trends continue, Micron could emerge as one of the most important — and potentially underappreciated — AI plays in the market.

For investors watching the AI boom unfold, MU stock may now deserve far more attention than it received during previous semiconductor cycles.